The Conversation (0)

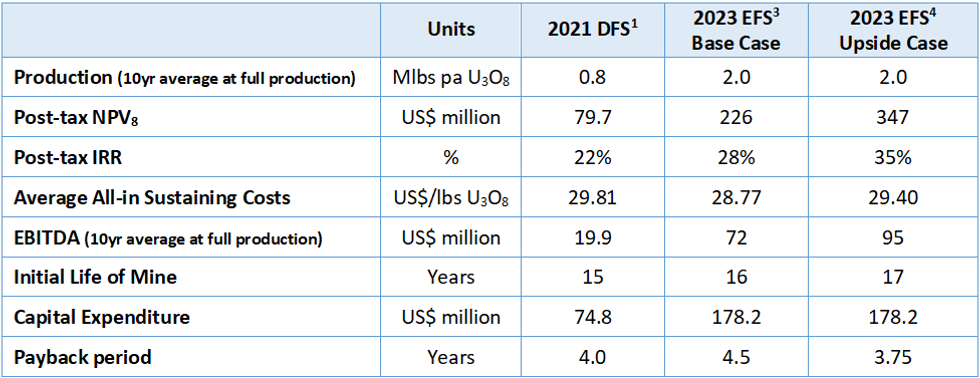

Aura Energy Limited (ASX: AEE, AIM: AURA, “Aura” or “the Company”) is pleased to announce the completion and delivery of the Enhanced Definitive Feasibility Study (“EFS”) for the Tiris Uranium Project (“Tiris” or the “Project”) in Mauritania. The EFS is based on the original 2021 study but now benefits from the recently updated Mineral Resource Estimate2 and revised throughput modelling that confirms an increase in steady-state production to 2.0 Mlbs pa U3O8 and the delivery of strong financial metrics and robust returns to shareholders over the life of the Project.

KEY POINTS:

- Average steady-state production increased by 150% from 0.8 Mlbs U3O8 to 2.0 Mlbs pa U3O8

- Strong financial metrics delivered from 60% of total Mineral Resources, headlined by a 180% increase in the Base Case post-tax NPV US$ 226M and IRR of 28%

- 57% cash margins from an AISC of US$ 28.77 / lb U3O8

- Initial capital cost of US$ 87.9 million with an additional capital of US$ 90.3 million to produce 2.0 Mlbs pa U3O8

- Government stakeholder agreement and major permits in place

- 16-year project life with near-term exploration upside

A proportion of the production target for the 2023 EFS is based on Inferred Mineral Resources. There is a low level of geological confidence associated with Inferred Mineral Resources, and there is no certainty that further exploration work will result in the determination of Indicated Mineral Resources or that the production target itself will be realised.

Commenting on the updated DFS, Aura Energy Managing Director Dave Woodall said:

“The EFS confirms the strong financial case for the Tiris Uranium Project. The Tiris Project is unique with its low capital intensity, low operating costs, competitive all-in-sustaining cost and key regulatory approvals in place. With a relatively short timeline for commercial production, the focus is now on the consideration of a Final Investment Decision as early as Q4 2023, which would see commissioning in late 2024 for commercial production in early 2025.

“What differentiates Tiris is the ore quality that allows free-dig shallow open pit mining. Aura does not require expensive drill and blast operations or capital-hungry infrastructure for crushing and screening. Following simple scrubbing and screening the Project will have a leach feed grade of >2,000 ppm U3O8 resulting in a downsizing of the leaching circuit that drives competitive operating costs and creates a competitive advantage for Aura Energy in a strengthening uranium market.”

Enhanced Definitive Feasibility Study Highlights

The key highlights from the EFS are:

- 150% increase in average steady-state production to 2.0 Mlbs U3O8

- Proven processing with simple free dig mining

- Rapid beneficiation that delivers >2,000 ppm U3O8 leach feed grade

- High confidence production scheduled with 76% Proved and Probable Reserves, and 24% Inferred Mineral Resources.

- Low initial capital cost and high capital efficiency from any future expansion

- Excellent cash margins driven by an AISC of US$ 28.77 / lb

- 18-month construction period provides rapid path to production following FID

- 15-year mine life with significant resource growth potential

The Tiris Uranium Project is located in the Tiris Zemmour region, an emerging uranium province approximately 1,450 km from the Mauritanian capital of Nouakchott. The Project is owned by Aura Energy, through its 85% owned Tiris Resources with its Mauritanian Government partner, the National Agency for Geological Research and Mining Heritage (ANARPAM).

The key differentiating feature of the EFS, compared to the 2021 DFS is the increase in production. The Project now plans to deliver a life of mine production of 25.5 Mlbs U3O8, an increase of 110%, taking advantage of the recently announced 52% increase in Measured and Indicated Resources to 29.6 Mlbs U3O8, (62.1Mt at 216 ppm U3O8, at a 100ppm grade cut-off).

The effect of this increased production is enhanced project economics, delivering a Base Case NPV8 of US$226 million, and an exceptional Base Case IRR of 28%, with further capacity to improve as nearby Resource growth, is targeted.

Beyond this Base Case Scenario, a long-term Upside Side was calculated using the Trade Tech Forward Availability Model (FAM2) forecast pricing of US$79/lb U3O8. This Upside Case forms the second scenario illustrated in this EFS demonstrating the leverage to forecast growth in the global uranium market by the World Nuclear Association. With an Upside Case NPV8 of US$347 million and a remarkable Upside Case IRR of 35%, this second scenario indicates that the Tiris Project could be one of the most exciting conventional mining uranium projects in development.

Further project optimisation will be investigated as part of the FEED study which has commenced using the outcomes of the EFS. Additional areas of optimisation within the recovery of the U3O8 are under investigation and require further engineering to optimise the production profile.

Click here for the full ASX Release

This article includes content from Aura Energy, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.

AEE:AU

Toro Energy

Overview

Countries worldwide are working towards decarbonization and paying more attention to clean energy sources. About 10 percent of the world's electricity is produced from 440 power reactors, and more countries like Japan, Germany, the UK and the US are revitalizing their nuclear energy capacities to reduce fossil fuel production while improving energy security.

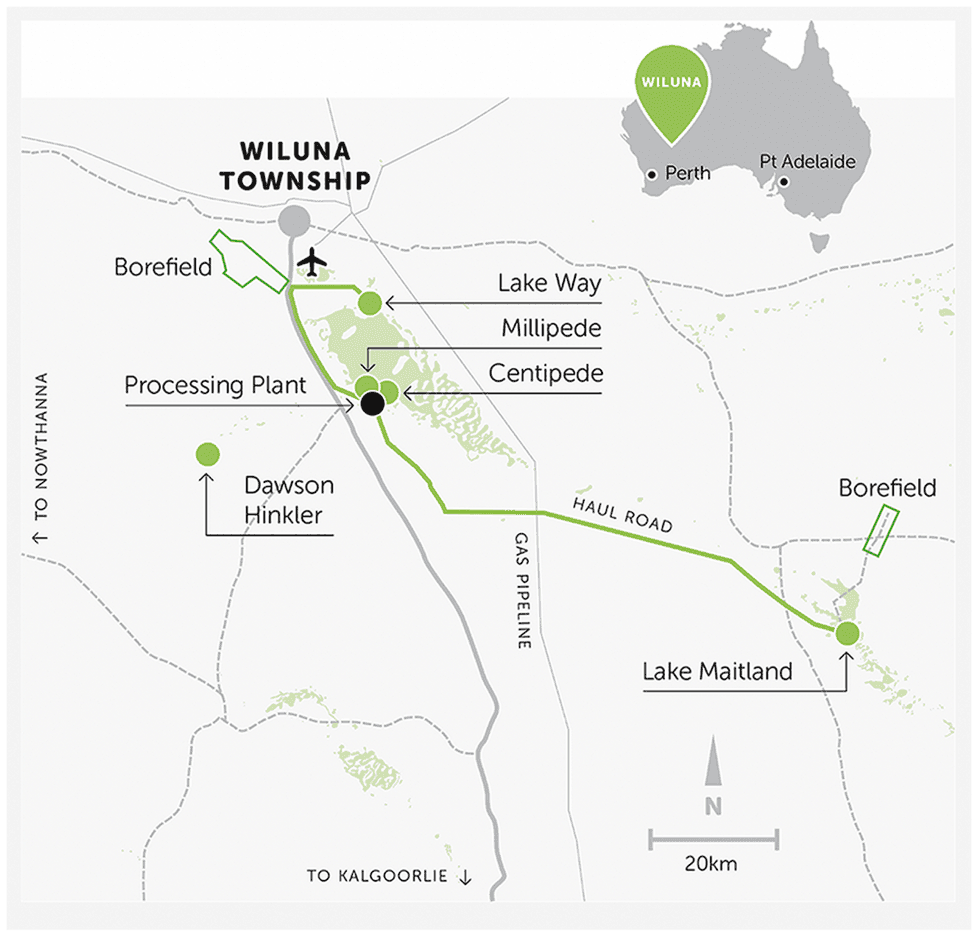

Australia produces 12 percent of the world’s uranium, behind Canada (13 percent) and Kazakhstan (43 percent). It is also home to the Wiluna uranium project, a well-established uranium resource, which is also the flagship asset of Toro Energy (ASX:TOE), a uranium exploration and development mining company that actively seeks to uncover value from other commodities in its existing highly prospective project ground.

Toro holds JORC-compliant uranium resources of 90.9 million pounds (Mlbs) uranium oxide (U3O8), at a 200 parts per million (ppm) U3O8 cut-off, across its Western Australia uranium projects, of which 84 Mlbs are proximally located within the northern goldfields region.

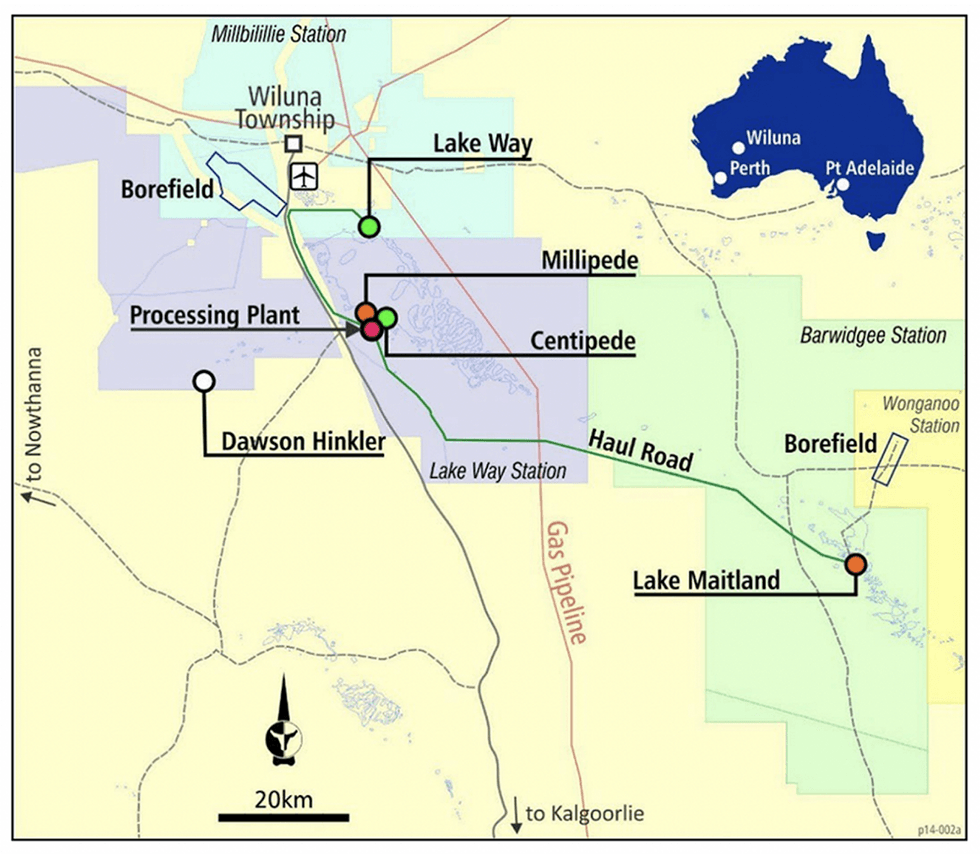

The 100-percent-owned Wiluna uranium project includes four key deposits – Lake Maitland, Centipede, Millipede and Lake Way – and offers significant uranium exposure of 52 million tons (Mt) @ 548 ppm for 62.7 Mlbs U3O8, at 200 ppm cut-off (JORC 2012). It is located only 30 kilometers southwest of Wiluna in Central Western Australia.

The Wiluna uranium project has received state and federal approval (subject to required amendments) and has been granted mining leases.

Considerable research over recent years has identified processing redesign opportunities from unique geological attributes within the uranium deposits, but particularly at Lake Maitland, as well as the ability to extract the inherent vanadium held within the uranium ‘ore’ for a vanadium by-product. Within the uranium mineralization envelope, the Wiluna project is estimated to contain 68.3 Mlbs of vanadium oxide (V2O5), inferred at 200 ppm V2O5 cut-off (JORC 2012).

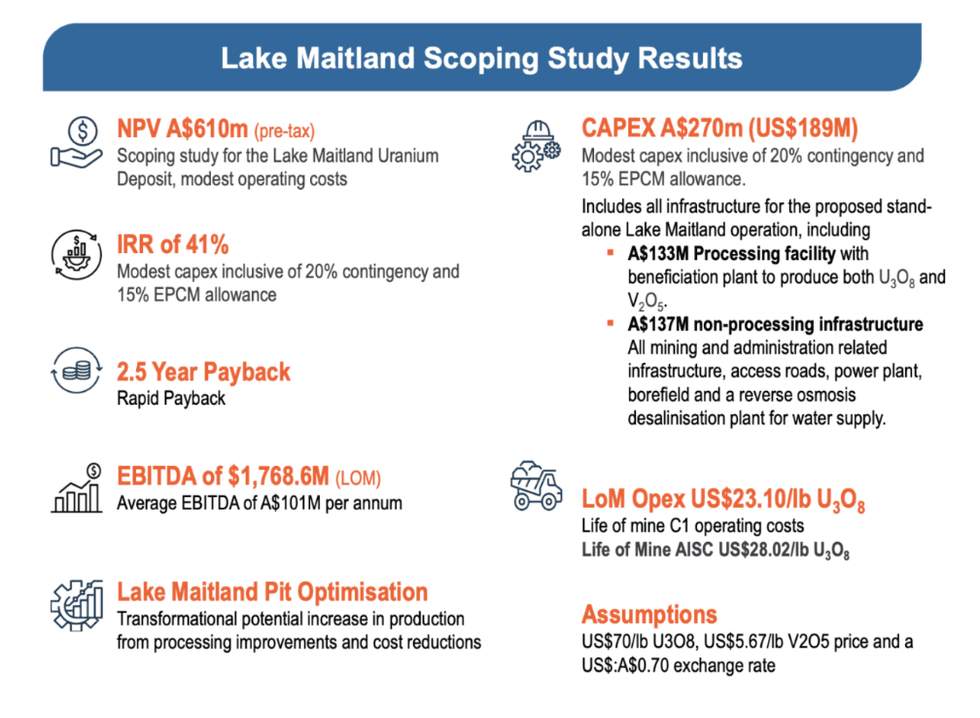

The unique geology of the Lake Maitland deposit and the processing redesign have allowed for a mining and processing option exclusively for Lake Maitland, that could be economic on its own or be the economic spearhead of a longer-term, larger Wiluna mining operation (dependent on market conditions and approvals). The stand-alone Lake Maitland option, aided by the economic efficiency of the new processing design, results in a transformational potential increase in production from the Lake Maitland deposit.

The scoping study for the stand-alone Lake Maitland uranium-vanadium operation option shows potential for exceptional financial returns with a pre-tax NPV of AU$610 million, a short payback period of 2.5 years, 41 percent internal rate of return, and low capital operating cost estimates (assuming an AU$/US$ exchange rate of 0.7 and US$70/lb U3O8 price and US$5.67/lb V2O5 price) after producing 22.8 Mlbs of U3O8 and 11.9 Mlbs of V2O5.

The Lake Maitland pit optimisation successfully increased potential production by 8Mlbs U3O8 and 11.9Mlbs V2O5 based on these assumptions.

The design phase of Toro Energy’s beneficiation and hydrometallurgical pilot plant is on track and in line with plans to begin operations in the second half of 2024. The pilot plant will test the improved beneficiation and hydrometallurgical circuit developed by Toro from bench scale research at a closer-to-production scale and as single streams. It will also test potential ore from the three uranium-vanadium deposits that Toro believes will make up an extended Lake Maitland operation – these include Lake Maitland, Lake Way and Centipede-Millipede.

The company will commence a large sonic core drill program to provide bulk, but targeted potential ore, for the upcoming pilot plant program.

Toro Energy has also recently initiated a refresh and update of its Lake Maitland scoping study using the latest, more favourable commodity pricing and exchange rate guidance.

The Lake Maitland deposit is part of a joint venture partnership with two reputable Japanese corporations, Japan Australia Uranium Resource Development. (JAURD) and Itochu.

Toro has been actively evaluating the prospectivity of its Wiluna asset portfolio for minerals other than uranium, including nickel and gold.

Toro’s Dusty nickel project is located on the northern, eastern and southern shores of Lake Maitland and the Lake Maitland uranium deposit and is focused on two main target areas: Dusty and Yandal One. These properties will be the subject of a proposed demerger, following Toro’s recent strategic review of its non-core assets and future plans to solely focus on its uranium development opportunities and its flagship Wiluna project.

Toro Energy’s management team and board of directors have extensive experience in the mining industry, with combined expertise that includes working at major mining houses, exploration companies, uranium mining operations, corporate financing and government and community relations.

Company Highlights

- Toro Energy is a well-established Western Australian uranium exploration and development company that actively seeks to uncover value from other commodities in existing highly prospective ground.

- Toro holds JORC-compliant uranium resources of 90.9 Mlbs U3O8 across its Western Australia uranium projects, of which 84 Mlbs is proximally located within the northern goldfields.

- Toro’s 100-percent-owned flagship Wiluna uranium project, located 30 kilometers southwest of Wiluna in Central Western Australia, contains 62.7 Mlbs of U3O8 at an average grade of 548 ppm over four deposits: Lake Maitland, Centipede, Millipede and Lake Way.

- The company has defined a significant maiden inferred vanadium resource of 68.3 Mlbs of V2O5 inside the uranium mineralisation envelope.

- Scoping Study completed for a stand-alone Lake Maitland Uranium-Vanadium operation shows potential for exceptional financial returns.

- In addition to its flagship uranium project, Toro’s strategic evaluation of the Lake Maitland tenure has resulted in the discovery of massive nickel sulphide and vein-hosted gold, which include the Dusty Nickel Project and the Yandal Gold Project.

- Following a recent strategic review, Toro is considering to solely focus on its uranium development opportunities and demerge its portfolio of non-core projects, including the nickel, gold and base metal assets in Western Australia.

- The company is led by a management team and board of directors with direct experience in the uranium exploration and mining as well as base metal exploration industry.

Key Projects

Wiluna Uranium Project

Toro Energy’s flagship asset is located only 30 kilometers from the town of Wiluna in the northern goldfields region within central Western Australia. The Wiluna project contains 62.7 Mlbs of U3O8 (at a 200 ppm U3O8 cut-off) over four deposits: Centipede, Millipede, Lake Way and Lake Maitland. The asset has been de-risked and optimized to improve yield and has successfully incorporated the processing of a vanadium resource as a by-product. A scoping study was completed for a stand-alone Lake Maitland uranium-vanadium operation.

Project Highlights:

- De-risked Uranium Project: Toro Energy has de-risked the Wiluna uranium asset by:

- Obtaining state and federal environmental approvals. Retrospective amendment to substantial commencement date condition will be required as well as amendment to mining proposal required as a result of further studies which significantly enhanced the project (refer below)

- Securing mining leases

- Identifying a simple yet effective mining process

- Drilling out the uranium resources so that the project’s JORC 2012-compliant 52 Mt at 548 ppm for 62.7 Mlbs of U3O8 (at a 200 ppm U3O8 cut-off) have a 96.3 percent measured and indicated status (JORC 2012)

- Extensive laboratory testing of a new and efficient beneficiation and processing technique inclusive of the extraction of vanadium for a valuable by-product.

- Uranium Exploration assets: Toro also owns 100 percent of three other exploration projects in Western Australia that have a total uranium resource of 28.2 Mlbs at Nowthanna, Dawson Hinkler and Theseus.

- Lake Maitland Pit Expansion: A 2022 pit expansion campaign, based on the new beneficiation and processing flow sheet and a stand-alone Lake Maitland mining operation, increased the potential of uranium ore and the asset by US$608 million in potential gross product value.

- Scoping study at proposed Lake Maitland Uranium-Vanadium Operation: Conducted by mining engineers at SRK Consulting Australasia, and metallurgical and processing engineers at Strategic Metallurgy, the scoping study results highlight the project’s potential for robust financial returns (assumes a US$70/lb U3O8, US$5.67/lb V2O5 price and a US$: AU$0.70 exchange rate).

- Scoping Study Financial Metrics Refresh: A refresh of the scoping study is underway to incorporate current financial metrics and improved uranium pricing.

- Further Expansion of Scoping Study: to incorporate amenable ore from Toro’s Lake Way and Centipede-Millipede uranium deposits into the proposed processing operation at Lake Maitland.

- Expanded Resource at Lake Way and Centipede-Millipede deposits: Expansion of the stated U3O8 and V2O5 resources at both the Centipede-Millipede and Lake Way uranium-vanadium deposits was conducted by reducing the stated U3O8 and V2O5 resource cut-off grades to 100 ppm (from 200 ppm):

- The stated Centipede-Millipede U3O8 resource expands by 25 percent or 5.98 Mlbs to 29.95 Mlbs contained U3O8, with a reduction in average grade to 351 ppm U3O8.

- The stated Lake Way U3O8 resource expands by 15 percent or 1.79 Mlbs to 14.12 Mlbs contained U3O8, with a reduction in average grade to 406 ppm U3O8.

- The stated Centipede-Millipede V2O5 resource expands by 17 percent or 6.6 Mlbs to 45.2 Mlbs contained V2O5, with a reduction in average grade to 281 ppm V2O5.

- The stated Lake Way V2O5 resource expands by 9.5 percent or 1.1 Mlbs to 12.7 Mlbs contained V2O5, with a reduction in average grade to 307 ppm V2O5.

- The Lake Maitland deposit will be re-estimated to better define the resource at the new cut-off grade before restating the resource and re-calculating the total Wiluna Project resources at the new cut-off grades of 100ppm.

- Pilot Plant Design Commissioned: A detailed pilot plant design is being undertaken to further assess the new processing flowsheet for Lake Maitland at a closer to ‘operational’ scale. The pilot plant design is on track incorporating all aspects of both uranium and vanadium production. A sonic core drilling program will commence to deliver potential ore to the pilot plant currently in design for Wiluna.

- Robust Local Infrastructure: The assets are within an established mining center, which means much of the required infrastructure is readily available. The project has access to power and water, which reduces initial development costs.

- Joint Venture Partnership: Toro Energy has entered into a joint venture partnership with JAURD and Itochu for its Lake Maitland deposit. Both corporations have the right, but not the obligation, to earn a combined 35 percent interest in the project upon contributing US$39.6 million, and an additional proportionate share of expenditure thereafter, once a positive final investment decision has been made based on a definitive feasibility study.

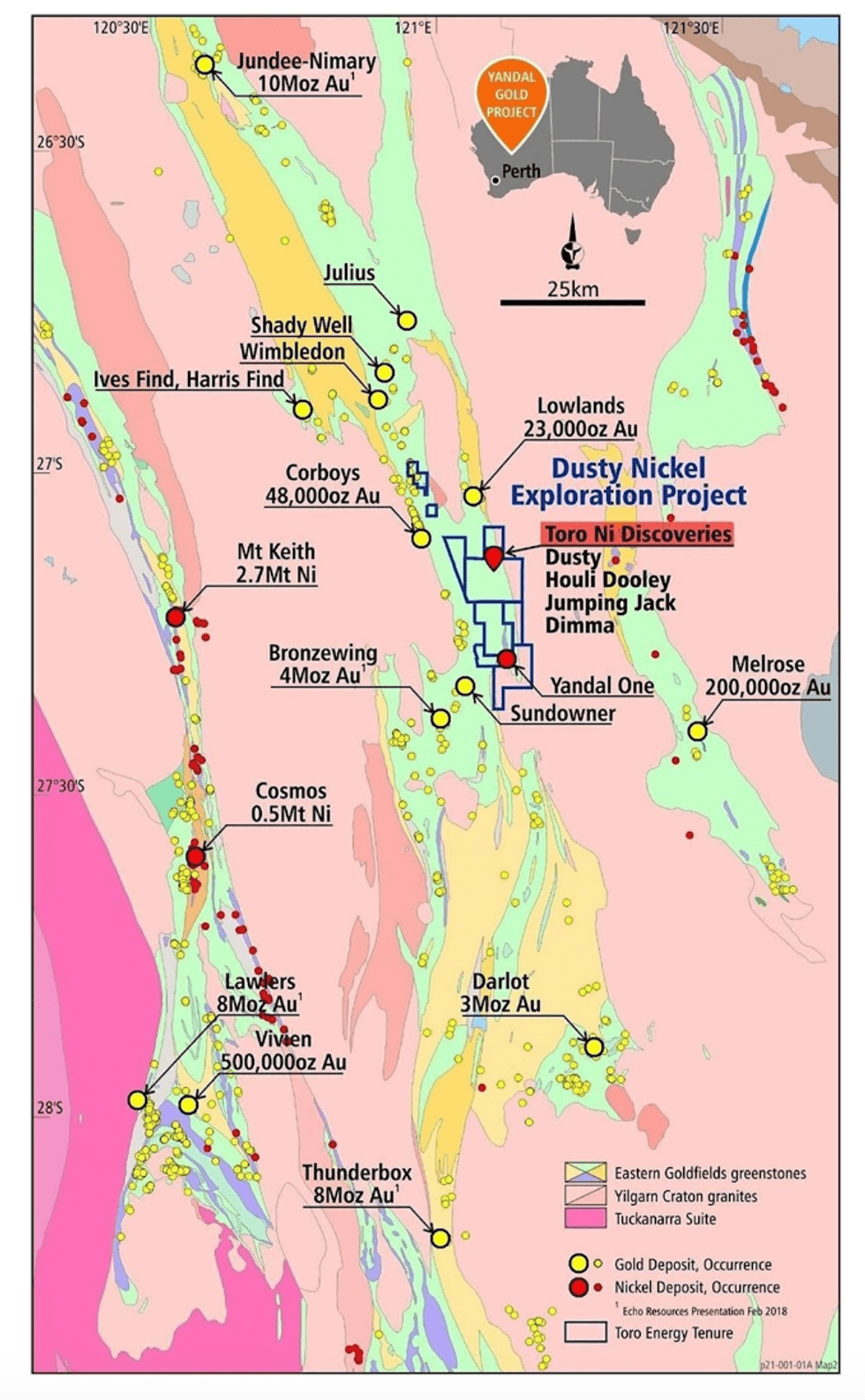

The Dusty Nickel Project – Discoveries of Massive Nickel Sulphide

Toro’s Lake Maitland tenure is located in the Yandal Greenstone Belt within the Yilgarn Craton of Western Australia, a gold district within a world-class gold and nickel province. With little exploration for non-uranium minerals ever conducted on the properties, Toro considers the project area highly prospective for nickel, gold and base metals.

In 2020, Toro made a blind discovery of massive and semi-massive nickel sulphides associated with the base of a 7.5-kilometer unbroken length of previously unknown komatiite (Dusty komatiite) – arguably the first massive nickel sulphides discovered in the Yandal Greenstone Belt, which is located 50 kilometers east of the world-class Mt. Keith nickel deposit. The Dusty nickel project is located near the Lake Maitland uranium deposit and contains two key target areas: Dusty and Yandal One.

Continued exploration and diamond drilling on the project has resulted in four discoveries of massive/semi-massive nickel sulphide zones to date with only 4.5 kilometers tested so far at a single depth along a 7.5-kilometer komatiite magnetic trend. Only limited testing for massive nickel sulphides has been undertaken to date of an approximately 15-kilometer strike length of known komatite - ultramafic target rock. With such limited drilling on the Lake Maitland tenure, it is yet to be known whether other similar magnetic anomalies are also komatiite-ultramafic rock and how much more rock is prospective for massive nickel sulphides on Toro’s 100-percent-owned Dusty nickel project.

Project Highlights:

- Four zones of massive nickel sulphide discovered: Toro has discovered four zones of massive and semi-massive nickel sulphides: Dusty, Houli Dooley, Jumping Jack and Dimma. Significant diamond drill results from these discoveries to date include:

- DUSTY

- 9 meters at 2.07 percent nickel from 250.9 meters downhole (TED07) including:

- 2.0 meter at 4.01 percent nickel from 250.9 meters downhole; and

- 2.0 meters at 3.85 percent nickel from 255.5 meters downhole.

- 2.6 meters at 3.45 percent nickel from 184.5 meters downhole (TED04).

- 7.2 meters at 1.05 percent nickel and 0.26 percent copper from 252 meters downhole (TED22).

- 9 meters at 2.07 percent nickel from 250.9 meters downhole (TED07) including:

- HOULI DOOLEY

- 3.05 meters at 1.59 percent nickel from 297.75 meters downhole (TED14).

- JUMPING JACK

- 3.45 meters at 1.42 percent nickel from 240.2 meters downhole (TED37).

- 2.44 meters at 1.16 percent nickel from 231.6 meters downhole (TED38).

- DIMMA

- 4.31 meters at 1.16 percent Ni from 243.3 meters downhole (TED41).

- 3.13 meters at 1.42 percent Ni from 314 meters downhole (TED42).

- 4.6 meters at 1.61 percent Ni from 194.2 meters downhole, including 3m at 1.09 percent Ni from 166 meters downhole (TED54).

- 2.1 meters at 1.83 percent Ni from 147.1 meters downhole (TED55).

- DUSTY

- Yandal OneTarget Area: The Yandal One Target Area is located some 17 kilometers south of the Dusty discoveries and with limited drilling, Toro has proven the existence of another komatiite with the potential to host massive nickel sulphide.

Toro Yandal Gold Project

The Lake Maitland tenure is located only 20 kilometers northeast of the world-class Bronzewing and Mt McClure gold mines within the same Greenstone Belt, the Yandal, within one of the most famous gold provinces in the world, the Yilgarn Craton.

Early exploration by Toro at the Golden Ways target area in the north of the project has uncovered surface rock chip samples of up to 70 g/t gold and significant drilling results, including:

- 5 meters at 4.4 g/t from 22 meters (TERC24)

- Including 2 meters at 9.93 g/t from 22 meters

- 4 meters at 3.3 g/t from 28 meters (TERC25)

- Including 1 meter at 10.9 g/t from 28 meters

- 2 meters at 3.79 g/t from 10 meters (TERC38)

- Including 1 meters at 7.33 g/t from 10 meters

- 3 meters at 1.41 g/t from 9 meters (TERC36)

- Including 1 meters at 2.76 g/t from 10 meters

Management Team

Richard Homsany - Executive Chairman

Richard Homsany has extensive experience in the resources industry, having been the executive vice-president for Australia of TSX-listed Mega Uranium since April 2010. He has worked for North Ltd, an ASX top 50-listed internationally diversified resources company in operations, risk management and corporate, before its takeover by Rio Tinto.

Homsany is an experienced corporate lawyer and certified practicing accountant (CPA) advising numerous clients in the energy and resources sector, including publicly listed companies. He was corporate partner at international law firm DLA Phillips Fox (now DLA Piper), where he advised clients on a range of transactions and matters including capital raising, IPOs, stock exchange listing, mergers and acquisitions, finance, joint ventures, divestments and governance.

He is a fellow of the Financial Services Institute of Australasia (FINSIA) and a member of the Australian Institute of Company Directors. He has a commerce degree and honors degree in law from the University of Western Australia, and a graduate diploma in finance and investment from FINSIA (State Dux).

Homsany has significant board experience with publicly listed companies in Australia and Canada. He is the chairman of ASX-listed copper explorer Redstone Resources. and TSXV-listed iron ore and gold explorer Central Iron Ore Limited. Homsany is currently the chairman of the Health Insurance Fund of Australia Limited.

Michel Marier - Non-executive Director

Michel Marier joined Sentient in 2009 as an investment manager. Before joining Sentient, Marier worked eight years in the private equity division of la Caisse de dépôt et placement du Québec. Marier holds a master’s degree in finance from HEC Montreal and is a CFA charter holder.

Richard Patricio - Non-executive Director

Richard Patricio is the CEO and president of Mega Uranium, a uranium-focused investment and development company with assets in Canada and Australia.

In addition to his legal and corporate experience, Patricio has built a number of mining companies with global operations. He holds senior officer and director positions in several junior mining companies listed on the TSX, TSX Venture, AIM and NASDAQ exchanges. He is currently also a director of NexGen Energy (TSE:NXE, Mkt Cap. C$2.7 billion). He previously practiced law at a top-tier law firm in Toronto and worked as an in-house general counsel for a senior TSX-listed company. He received his law degree from Osgoode Hall and was called to the Ontario bar in 2000.

Katherine Garvey - Legal Counsel and Company Secretary

Katherine Garvey is a corporate lawyer who has significant experience in the resources sector. Garvey advises public (both listed and unlisted) and proprietary companies on a variety of corporate and commercial matters including capital raising, finance, acquisitions and disposals, Corporations Act and ASX Listing Rule compliance, corporate governance and company secretarial issues. She has extensive experience drafting and negotiating various corporate and commercial agreements including farm-in agreements, joint ventures, shareholders’ agreements, and business and share sale and purchase agreements.

Garvey is a senior associate at Cardinals Lawyers and Consultants, a corporate and resources law firm in West Perth, and company secretary of the Health Insurance Fund of Australia Limited. Garvey is also legal counsel (Australia) to TSX-listed Mega Uranium, and company secretary to TSXV-listed Central Iron Ore.

Dr. Greg Shirtliff – Geology Manager

Dr. Greg Shirtliff has over 20 years of experience in industry-related geology and geochemistry, including a PhD in mine-related geology and geochemistry from the Australian National University. Since his studies, Dr Shirtliff has spent over 17 years in various roles in the mining and exploration industry ranging from environmental, mine geology, resource development, exploration and management roles in exploration and technical projects inclusive of engineering and metallurgical. His roles have included a number of years at ERA-Rio Tinto’s Ranger Uranium Mine, as the senior geoscientist for Cameco Australasia and more recently as the lead geologist and technical manager for Toro Energy, where he is the exploration and technical lead responsible for increasing the viability of the company’s uranium and mineral resources, developing and directing the company’s uranium and non-uranium exploration strategy, aiding the company technically through EPA approval for a uranium mine, and guiding the engineering and metallurgical through to scoping level economic assessment.

Dr Shirtliff has had recent exploration success at Toro Energy, discovering multiple zones of massive nickel sulphide mineralization along the Dusty Komatiite, arguably the first massive nickel sulphide mineralization discovered in the Yandal Greenstone Belt in Western Australia.

Dr Shirtliff holds directorships on privately owned consultancy and prospecting companies and is a long-standing member of the Australian Institute of Mining and Metallurgy and the internationally recognized Society of Economic Geologists.

Marc Boudames - Financial Controller

Marc Boudames is experienced in statutory financial reporting, taxation, ERP systems, business analytics, corporate transactions, due diligence, mergers & acquisitions, finance, joint ventures and divestments. He previously worked at RSM Bird Cameron, as general manager –finance & administration for ASX-listed Redport Ltd and Mega Uranium (Australia), a Canadian TSX-listed mining and equity investment company focused on global uranium properties and multi-mineral exploration. He has worked for multiple companies across various industries, including listed and public companies associated with the mining and oil and gas sectors, such as WesTrac, CB&I and Spotless Group.

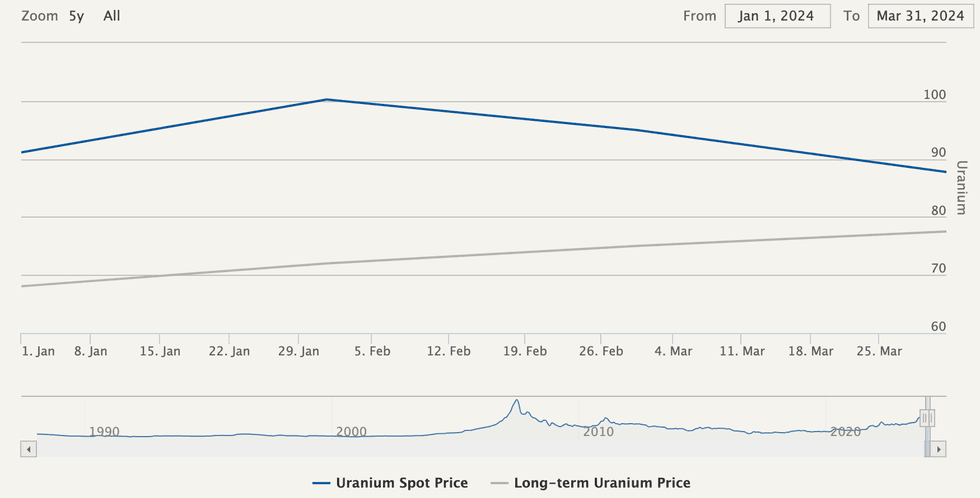

Uranium Price Update: Q1 2024 in Review

These favorable fundamentals are expected to support uranium prices for the remainder of the year.

Finegold also noted that spot market activity highlights how sensitive the sector is to supply challenges.

“Spot market prices have also been a key talking point as volatility in pricing has increased dramatically in Q1 to both the upside and downside,” he explained. “It has brought to light just how thinly traded the spot market is, but interestingly term prices have only continued to rise, which is indicative that the long-term fundamentals remain intact.”

Sulfuric acid shortage impeding supply growth

The U3O8 spot price opened the year at US$91.71 and edged higher through January 22, when values hit a 17 year high of US$106.87. However, the near two decade record was short lived, and by month’s end uranium was around US$100.

Uranium price, Q1 2024.

Chart via Cameco.

Some of the price positivity early in the quarter came as Kazatomprom (LSE:KAP,OTC Pink:NATKY) warned that it was expecting to adjust its 2024 production guidance due to “challenges related to the availability of sulfuric acid.”

The state producer and major uranium player confirmed the reduction on February 1, underscoring the importance of sulfuric acid in its in-situ recovery method and describing its efforts to secure supply.

“Presently, the company is actively pursuing alternative sources for sulfuric acid procurement,” a press release states.

“Looking ahead in the medium term, the deficit is expected to alleviate as a result of the potential increase in sulphuric acid supply from local non-ferrous metals mining and smelting operations. The company also intends to enhance its in-house sulfuric acid production capacity by constructing a new plant.”

In 2023, Kazatomprom initiated the establishment of Taiqonyr Qyshqyl Zauyty to oversee the construction of a new sulfuric acid plant capable of producing 800,000 metric tons annually.

In the years ahead, the company is aiming to bolster its sulfuric acid production capacities through existing partnerships to achieve a consolidated production volume of approximately 1.5 million metric tons.

In the meantime, disruptions to Kazakh output will only grow the market deficit.

According to the World Nuclear Association, total global uranium production in 2022 only satiated 74 percent of global demand, a number that is likely to shrink as nuclear reactors in Asian countries begin coming online.

“Kazakhstan is the largest producer of uranium in the world — 44 percent. We like to think of Kazakhstan as the OPEC of uranium,” John Ciampaglia, CEO of Sprott Asset Management, said during a recent webinar.

Kazatomprom forecasts its adjusted uranium production for 2024 will range between 21,000 and 22,500 metric tons on a 100 percent basis, and 10,900 to 11,900 metric tons on an attributable basis. While in line with the company’s 2023 output, the major had to forgo a production ramp up due to the sulfuric acid shortage and development issues.

Analysts and market watchers foresee the sulfuric acid shortage being a long-term price driver.

“The sulfuric acid issue in Kazakhstan is a systemic problem that we do not believe will go away any time soon,” said Finegold. “While the company is doing what they can to alleviate pressures on sulfuric acid supplies, we believe their ability to ramp up production will be hindered for several years before their third domestic plant comes online. As such, we do not see Kazakh uranium production increasing significantly over the next three to four years.”

COP28 nuclear commitment supporting demand

The U3O8 spot price spiked again in early February, reaching US$105 before another correction set in.

As Finegold explained, some of the retraction was the result of profit taking from short-term holders.

“Financial speculators looking to lock in profits towards March year ends played a role, but as we know these moves are achieved on very little volume, so the point remains that the long-term thesis remains unchanged,” he said.

Finegold went on to highlight the different investment perspectives within the market.

“Spot market participants trade on very different parameters and time horizons to one another,” he said. “A trader and a hedge fund, for example, act in a totally different manner to a utility who are long-term thinkers.”

Despite February's slight contraction, uranium prices have remained elevated above US$80.

Some of this long-term support is the result of a COP28 nuclear capacity declaration. At the organization's December meeting in Dubai, more than 20 countries signed a proclamation to triple nuclear capacity by 2050.

There are currently 440 operational nuclear reactors with an additional 13 slated to come online this year and another 47 expected to start electricity generation by 2030. For Finegold, this commitment to building and fortifying nuclear capacity has been uranium's most prevalent demand trend. “The demand side of the equation remains robust and growing at a time when the supply side has never been more fragile,” he commented.

Others also believe the COP28 commitment was a tipping point for the uranium market that spawned several announcements about mine restarts and project extensions.

“Governments around the world have acknowledged that they need to be more supportive, not just financially, but in terms of expediting new projects, expediting the environmental permitting processes for new uranium mines,” said Sprott’s Ciampaglia during the webinar. “And it's not just happening in one country — with the exception of one or two outliers in Europe, this is happening around the globe.”

Geopolitical risk and resource nationalism are price catalysts

Uranium prices continued to consolidate from mid-February through mid-March, but remained above US$84.

This positivity saw several uranium companies in the US, Canada and Australia announce plans to bring existing mines out of care and maintenance. In late November, uranium major Cameco (TSX:CCO,NYSE:CCJ) announced it was restarting operations at its McArthur River/Key Lake project in Saskatchewan after four years.

In January, the McClean Lake joint venture which is co-owned by Denison Mines (TSX:DML,NYSEAMERICAN:DNN) and Orano Canada, reported plans to restart its McClean Lake project, also located in the Athabasca Basin of Saskatchewan.

South of the border, exploration company IsoEnergy (TSXV:ISO,OTCQX:ISENF) is gearing up to restart mining at its Tony M underground mine in Utah. “With the uranium spot price now trading around US$100 per pound, we are in the very fortunate position of owning multiple, past-producing, fully permitted uranium mines in the U.S. that we believe can be restarted quickly with relatively low capital costs," IsoEnergy CEO and Director Phil Williams said in a February release.

Building North American capacity is especially important ahead of the global nuclear energy ramp up and the ongoing geopolitical tensions between Russia and the west. While nuclear power is used to provide nearly 20 percent of America's electricity, the nation produces a very small amount of the uranium it needs.

Instead, the country imports as much as 40.5 million pounds annually.

According to the US Energy Information Administration, 27 percent of imports come from ally nation Canada, while 25 percent of imports come from Kazakhstan and 11 percent originate in Uzbekistan — both considered allies of Russia.

Commenting on that topic, Finegold noted, “The ongoing talk around US sanctions remains the most significant geopolitical catalyst for the sector." He added, "While we do not believe sanctions could be enforced immediately, it will send a signal to the market that Russia will no longer be involved in the largest uranium market in the world and would inevitably have an impact on fuel cycle component prices.”

If sanctions do limit imports from Russian allies, Finegold expects these countries to form stronger ties to China.

“Outside of this, the relationship between Kazakhstan and China remains one to watch as the Chinese continue their nuclear rollout strategy and look to procure millions of Kazakh-produced pounds,” he added.

Uranium price outlook remains positive

After hitting a Q1 low of US$84.84 on March 18, uranium began to move positively, ending the three month session in the US$88 range. Commitments to nuclear capacity, the energy transition and stifled supply will continue to be the most prevalent market drivers heading into the second quarter and the rest of the year.

“We believe uranium prices will significantly outrun the recent US$107 highs from February in 2024, driven by a fundamental supply/demand imbalance,” said Finegold. “Producers will continue to cover production shortfalls, while utilities struggle to replenish inventory shortages.”

The Ocean Wall associate went on to note, “The inherent appetite of traders and financial speculators will continue to drive prices higher. These demand drivers are converging at a time when supply has never looked more fragile.”

Don’t forget to follow us @INN_Resource for real-time updates!

Securities Disclosure: I, Georgia Williams, hold no direct investment interest in any company mentioned in this article.

Editorial Disclosure: The Investing News Network does not guarantee the accuracy or thoroughness of the information reported in the interviews it conducts. The opinions expressed in these interviews do not reflect the opinions of the Investing News Network and do not constitute investment advice. All readers are encouraged to perform their own due diligence.