The Conversation (0)

Lake Resources NL has received a vote of confidence from authorities in Argentina, reaffirming their support for lithium development and exploration.

Highlights:

- Meetings in Argentina with the provincial governor and regulators reaffirmed support for Lake’s flagship Kachi Lithium Brine Project, as well as other projects.

- Argentina’s three lithium provinces and new federal government continue to seek new export income sources, including the resources sector.

Lithium explorer and developer Lake Resources NL (ASX:LKE) has received a vote of confidence from authorities in Argentina, with meetings with provincial governors and regulators reaffirming their support for lithium development and exploration, including Lake’s Kachi Lithium Brine Project in Catamarca Province.

The meetings, held with governors and regulators in Jujuy, Catamarca and in Buenos Aires, focused on the need to secure new forms of export income in each of the lithium provinces and under the direction of the new federal government. This included support for lithium development and exploration, while ensuring environmentally and socially responsible development in line with international best practice. This follows similar comments made in meetings prior to the recent elections.

The recent talks included members of Lake’s local subsidiary, Morena del Valle S.A, a company established in Catamarca which employs primarily local people.

Lake’s Managing Director Steve Promnitz said: “We are pleased with the continued support of regulators and government in the provinces in which we operate in Argentina and it clearly demonstrates their commitment to supporting more foreign investment in the sector when local concerns are recognised. As shareholders are aware, recent national elections in Argentina have resulted in a change of party and leadership and ongoing support from new members of government is always important.

“Such support is vital as Lake moves towards the development of what is undoubtably a very large new lithium project at Kachi based on a potentially groundbreaking direct extraction process, which offers the potential for a smaller environmental footprint without requiring evaporation ponds.”

On 9 January (refer ASX announcement 9 Jan 2020), Lake announced that a battery grade lithium carbonate with 99.9% purity had been produced with very low impurities using partner Lake Solutions’ disruptive technology in California. This exceeded the standard 99.5% purity required for battery grade, which together with minimal impurities such boron represented a potential major breakthrough for the lithium brine industry. Lake now plans to dispatch samples to potential downstream off-takers, for the purpose of securing binding offtake agreements for Kachi brine products.

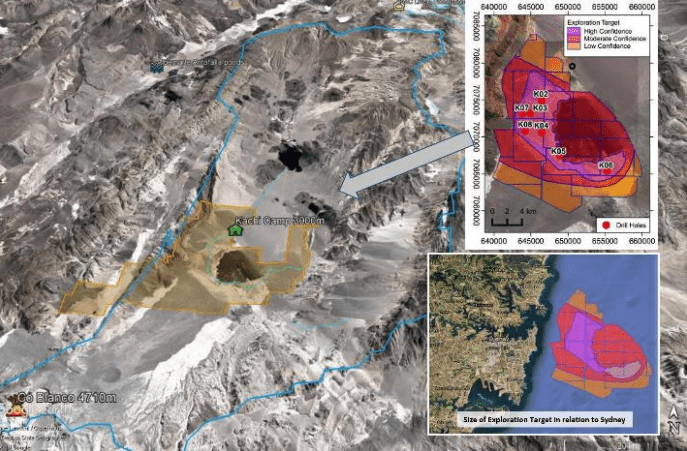

The Kachi project ranks amongst the world’s top 10 lithium brine resources. The mining leases cover over 70,000 hectares. By comparison, the target covers an area more than a third of the Sydney basin (Fig.2). Kachi has a maiden resource estimate of 4.4 million tonnes lithium carbonate equivalent (LCE) (Indicated 1.0 Mt and Inferred 3.4 Mt) within a much larger target (refer ASX announcement 27 November 2018).

Figure 1: The new governor of Catamarca, Raúl Jalil, the new Minister for Mining, Rodolfo Micone, senior cabinet members and Lake’s Steve Promnitz discussing company progress as reported in the local media. Copyright Ⓒ El Esquiú.

Figure 2: Kachi Lithium Project showing mining lease boundaries (yellow) covering 70,000 hectares at the lowest point of a large drainage basin of 6,800km2 (blue line) with insets showing the target size in relation to the Sydney basin (from ASX announcement 31 Jan 2019).

About Lake Resources NL (ASX:LKE)

Lake Resources NL (ASX:LKE, Lake) is a lithium exploration and development company focused on developing its three lithium brine projects and hard rock project in Argentina, all owned 100%. The leases are in a prime location among the lithium sector’s largest players within the Lithium Triangle, where half of the world’s lithium is produced at the lowest cost. Lake holds one of the largest lithium tenement packages in Argentina (~200,000Ha) secured in 2016 prior to a significant ‘rush’ by major companies. The large holdings provide the potential to provide consistent security of supply, scalable as required, which is demanded by battery makers and electric vehicle manufacturers.

The Kachi project covers 70,000 ha over a salt lake south of FMC/Livent’s lithium operation and near Albemarle’s Antofalla project in Catamarca Province. Drilling at Kachi has confirmed a large lithium brine bearing basin over 20km long, 15km wide and 400m to 800m deep. Drilling over Kachi (currently 16 drill holes, 3100m) has produced a maiden indicated and inferred resource of 4.4 Mt LCE (Indicated 1.0Mt and Inferred 3.4Mt) (refer ASX announcement 27 November 2018).

A direct extraction technique is being tested in partnership with Lilac Solutions, which has shown 80-90% recoveries and lithium brine concentrations 30-60,000 mg/L lithium. Battery grade lithium carbonate has been produced from Kachi brine samples with very low impurities (Fe, B, with <0.001 wt%). Phase 1 Engineering Study results have shown operating costs forecast in the lowest cost quartile (refer ASX announcement 10 December 2018). Test results have been incorporated into a Pre-Feasibility Study (PFS) aimed to be released soon. The Lilac process is being trialed with a pilot plant in California which will then be transported to site to produce larger battery grade lithium samples. Discussions are advanced with downstream entities, mainly battery/cathode makers, as well as financiers, to jointly develop the project.

The Olaroz-Cauchari and Paso brine projects are located adjacent to major world class brine projects either in production or being developed in the highly prospective Jujuy Province. The Olaroz-Cauchari project is located in the same basin as Orocobre’s Olaroz lithium production and adjoins the Ganfeng Lithium/Lithium Americas Cauchari project, with high grade lithium (600 mg/L) with high flow rates drilled immediately across the lease boundary.

The Cauchari project has shown lithium brines over 506m interval with high grades averaging 493 mg/L lithium (117-460m) and high flow rates, with up to 540 mg/L lithium. These results are similar to lithium brines in adjoining pre-production areas under development and infer an extension and continuity of these brines into Lake’s leases (refer ASX announcements 28 May, 12 June 2019).

Significant corporate transactions continue in adjacent leases with development of Ganfeng Lithium/Lithium Americas Cauchari project with Ganfeng announcing a US$237 million for 37% of the Cauchari project previously held by SQM, followed by a further US$160 million to increase Ganfeng’s equity position to 50% on 1 April 2019, together with a resource that had doubled to be the largest on the planet. Ganfeng then announced a 10 year lithium supply agreement with Volkswagen on 5 April 2019. Nearby projects of Lithium X were acquired via a takeover offer of C$265 million completed March 2018. The northern half of Galaxy’s Sal de Vida resource was purchased for US$280 million by POSCO in June-Dec 2018. LSC Lithium was acquired in Jan-Mar 2019 for C$111 million by a mid-tier oil & gas company with a resource size half of Kachi. These transactions imply an acquisition cost of US$55-110 million per 1 million tonnes of lithium carbonate equivalent (LCE) in resources.

For more information on Lake, please visit https://www.lakeresources.com.au/home/

Click here to connect with Lake Resources NL (ASX:LKE) for an Investor Presentation