GTI Energy Ltd (GTI or Company) is pleased to advise that 2 mud rotary drill rigs have now completed the first 25 holes, for 12,820-feet (3,908 metres), of its planned 100,000-foot drill program in Wyoming’s Great Divide Basin. Drilling has commenced within the Thor prospect (Thor) with 40,000-feet (12,200 metres) for ~70-holes of drilling planned at Thor (Figure 2).

Highlights

Two rigs in operation at GTI’s Thor ISR uranium prospect

First 25 holes completed of the 40,000ft (~12,200m) ~70-hole drill program

17 out of 25 holes met or exceeded the target uranium grade cut-off

Mineralisation conducive to ISR recovery with water table 100-200 ft above host sands

1,830 ft of new mineralised roll fronts found to date for a total of 19,470 ft (3.69 miles)

Drilling has commenced at the Thor prospect (Thor), located adjacent to Ur-Energy Inc’s (URE) 18Mlb Lost Creek uranium deposit and operating ISR uranium processing plant2. Exploration at Thor previously identified mineralisation with economic potential based on widths, grades & depth of mineralisation (ASX release 29 March 2022)1. An initial 100-hole (~50,000 ft) drilling campaign was completed at Thor from November 2021 – March 2022. As part of GTI’s 2022 100,000-foot drill program, a 70-hole follow-up campaign is underway to target extents of approximately 2 miles of mineralised uranium roll fronts at the Thor Project.

Twenty-five holes were completed to date of a planned 70-hole (~40,000 ft) program. Drilling is focused in the north-east of Thor, including fresh ground at the two state leases (Figures 2 & 4).

25 holes were completed for a Thor for total of 12,820 feet (3,908 metres) of drilling (Figures 2 & 4). Typical economically viable ISR grade and GT cut-offs are: 0.02% (200ppm) U3O8 and 0.2GT i.e., 10 ft (3 m) @ .02% (200ppm) U3O8. Initial results (Tables 1 & 2) are observed as follows:

11 of 25 holes met both grade and GT cutoff with an average of 0.49GT

7 of the remaining holes met grade cutoff but not GT, 4 had trace mineral & 3 were barren

Executive Director Bruce Lane commented“Results from the first 25 holes strongly justify this follow-up campaign at Thor. The historical drill maps combined with interpretation from our previous drilling have generated a high strike rate. The mineralisation identified continues to show potential for ISR development as we extend our understanding of the roll fronts and work towards a resource report. We look forward to continuing exploration over the coming weeks and months when conditions for US domestic uranium, particularly in Wyoming, continue to strengthen.”

This article includes content from GTI Energy Ltd, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.

Wyoming has the largest uranium reserves of all the US states and is the home of in-situ recovery (ISR) uranium mining, with experimental ISR mining during the early 1960s and commercial ISR mining starting in 1974. The state is an energy powerhouse in the US, second only to Texas in energy production and accounting for more than 80 percent of the country’s uranium production. It has a production history that dates back to the late 1940s. With a soaring uranium price that passed $90 by the end of 2023, many analysts believe the price will remain on the higher end for years to come.

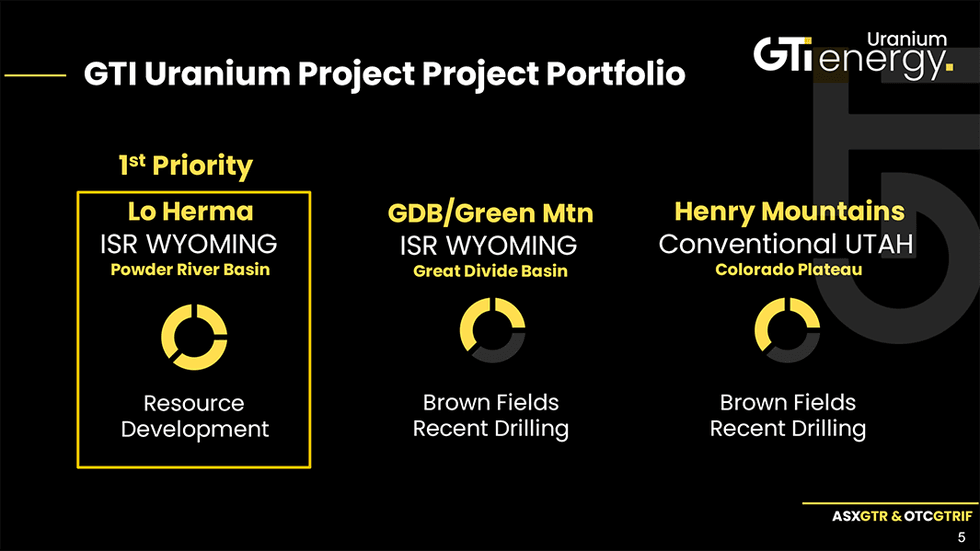

GTI Energy (ASX:GTR, OTCQB:GTRIF) is a mineral exploration company focused on developing a portfolio of attractive uranium projects in the United States. The company now boasts approximately 42,000 acres in the prolific Great Divide and Powder River Basins, which are low-cost ISR uranium-producing districts within 100 miles of each other.

In 2022, the company completed an additional 103 mud rotary exploration drill holes to increase the total trend length for GTI’s projects in the Great Divide Basin to 7.5 miles.

The company has also commenced work at its Green Mountain ISR uranium project next to Rio Tinto’s (ASX:RIO) uranium deposits. GTI has historical drill data confirming the presence of uranium mineralised roll fronts on the properties.

The company is led by a highly experienced management and exploration team with an extensive track record in the mineral exploration industry. GTI’s operational team has proven development and engineering expertise with a history of success in ISR uranium deposit discovery in Wyoming.

GTI’s acquisition of Branka Minerals in November 2021 gave the company control of the largest non-US or Canadian-owned uranium exploration landholding in the Great Divide Basin, with approximately 19,500 acres. The landholding included underexplored and highly prospective sandstone-hosted uranium properties which are the company’s Wyoming projects today. This holding then grew with the purchase of the 13,800-acre Green Mountain project in 2022.

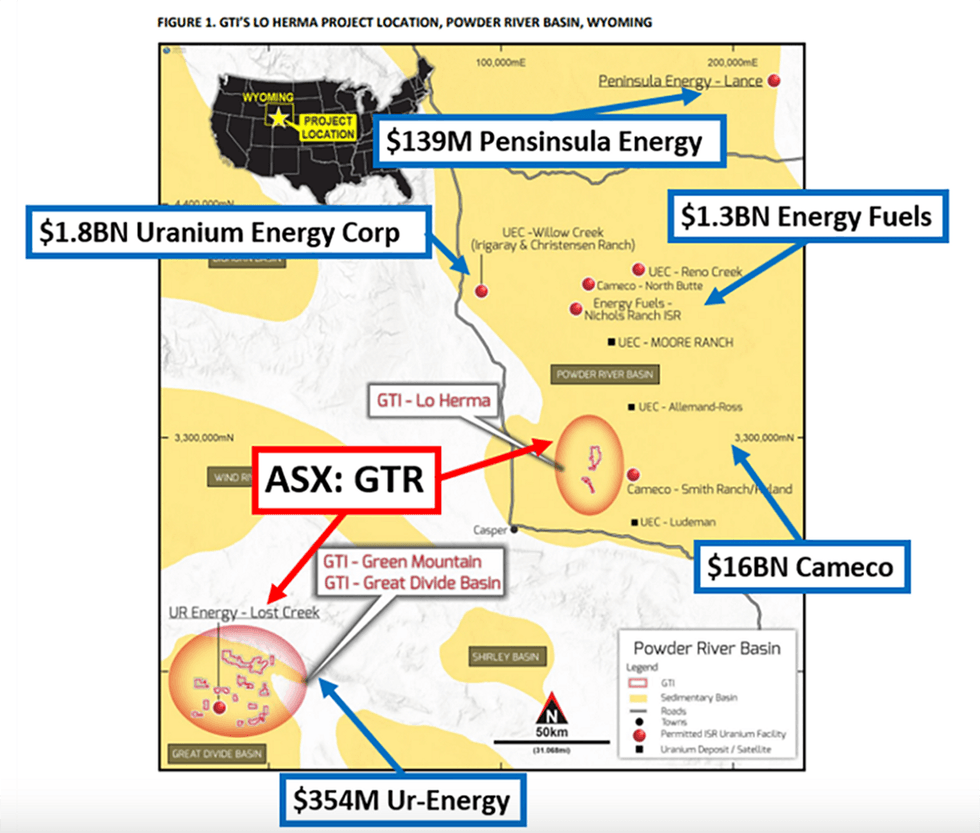

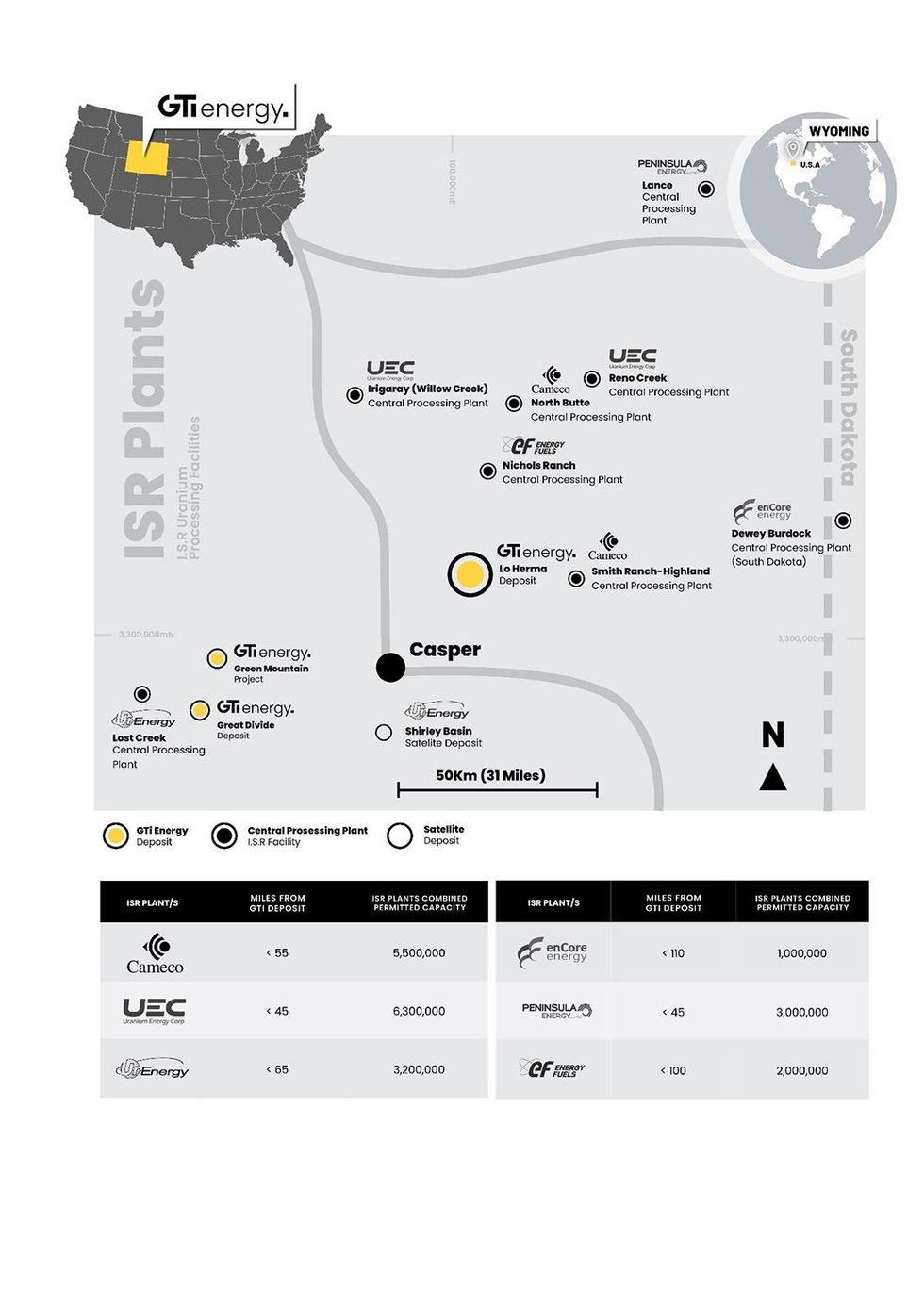

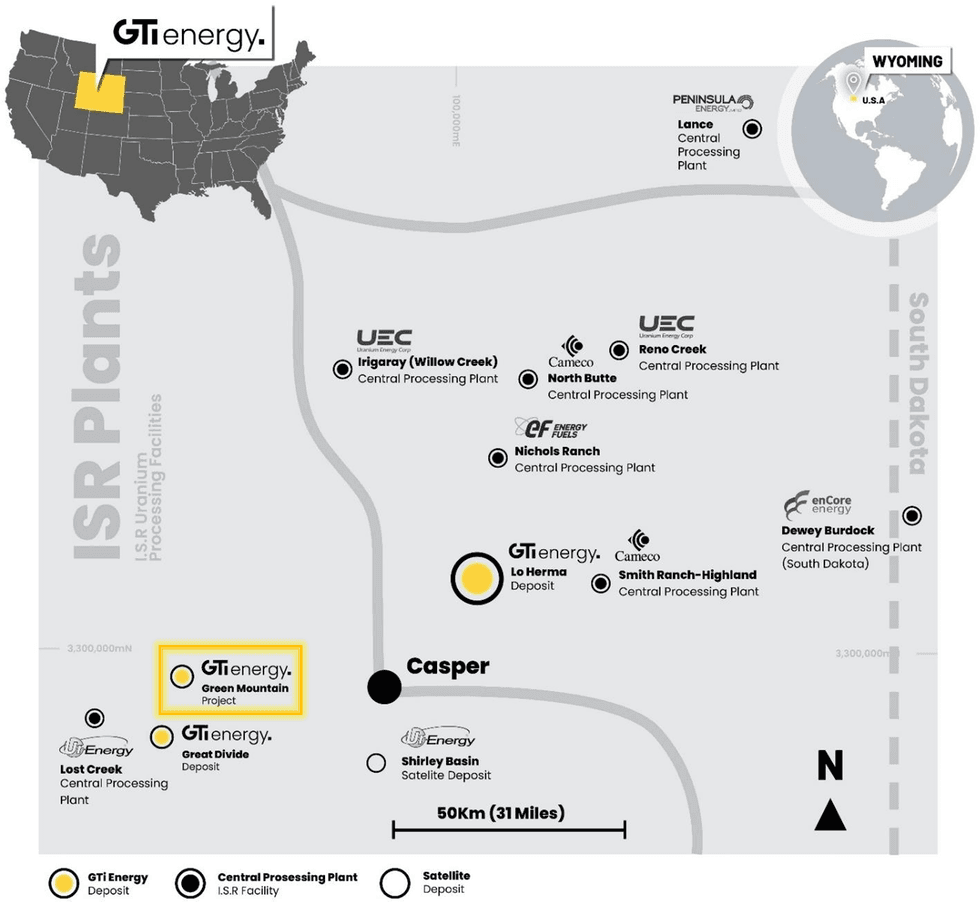

The company further expanded its ISR uranium portfolio in 2023 by acquiring the Lo Herma Project in Wyoming’s prolific Powder River Basin uranium district. The newly staked 13,300 acres of claims are located within 16 kilometers of Cameco’s Smith Ranch-Highland ISR uranium production plant – the largest production site in Wyoming

GTI Energy leverages the strategic positioning of its Wyoming projects, which are located near Ur Energy’s (TSX:URE,NYSE:URG) Lost Creek ISR production plant and the now-rehabilitated historic Rio Tinto Kennecott Sweetwater Mill. The Lost Creek plant is claimed by Ur Energy to be the lowest-cost ISR uranium production plant outside of Kazakhstan.

GTI is committed to strong environmental, social and governance (ESG) initiatives to support the clean energy transition. In November 2021, the company adopted an internationally recognized Environmental, Social and Governance Stakeholder Capitalism Metrics framework, with 21 core metrics and disclosures.

In December 2021, GTI Energy announced it would be transitioning to carbon-neutral operations. The company has subsequently received its carbon neutral certification for its Australian head office and US field operations, through the Australian Government’s Climate Active Program.

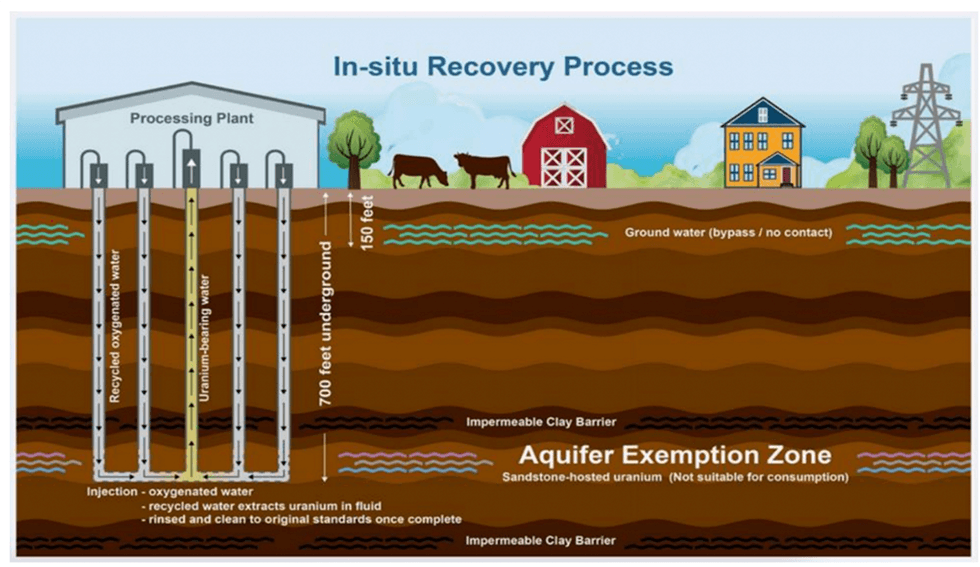

GTI Energy is positioned for growth with the pursuit of ISR mining on its Wyoming projects, presenting an opportunity for low operating expenses and capital expenditures with low environmental impact compared to conventional mining. ISR mining supports the company’s goal of low-impact mining and carbon neutrality on its Wyoming projects.

In 2021, the company completed field exploration on its Henry Mountains project in Utah. In the same year, GTI Energy also began a 15,000-meter drill program on its Wyoming projects, concluding the program in early 2022. The drilling confirmed that the targeted ISR-amenable uranium mineralization was present at the Thor project. In 2022, the company completed an additional 103 mud rotary exploration drill holes to increase the total trend length for GTI’s projects in the Basin to 7.5 miles.

Company Highlights

GTI Energy owns multiple promising assets in Wyoming’s prolific and in-situ recovery (ISR) uranium-producing Great Divide and Powder River Basins. Wyoming is the leading US uranium production state and is “uranium-friendly”.

GTI’s flagship Lo Herma project comprises 13,300 acres of ground in Wyoming within circa 16 kilometers of Cameco’s $16-billion ISR uranium plant (the largest permitted ISR production facility in Wyoming) and 80 kilometers of five permitted ISR uranium production facilities, including UEC’s Christensen Ranch (due to restart in August 2024) and Peninsula Energy’s (ASX:PEN) Lance Project (due to recommence production in late 2024).

GTI’s Great Divide Basin projects are strategically located near Ur Energy’s (TSX:URE,NYSE:URG) Lost Creek ISR production plant which has re-commenced production.

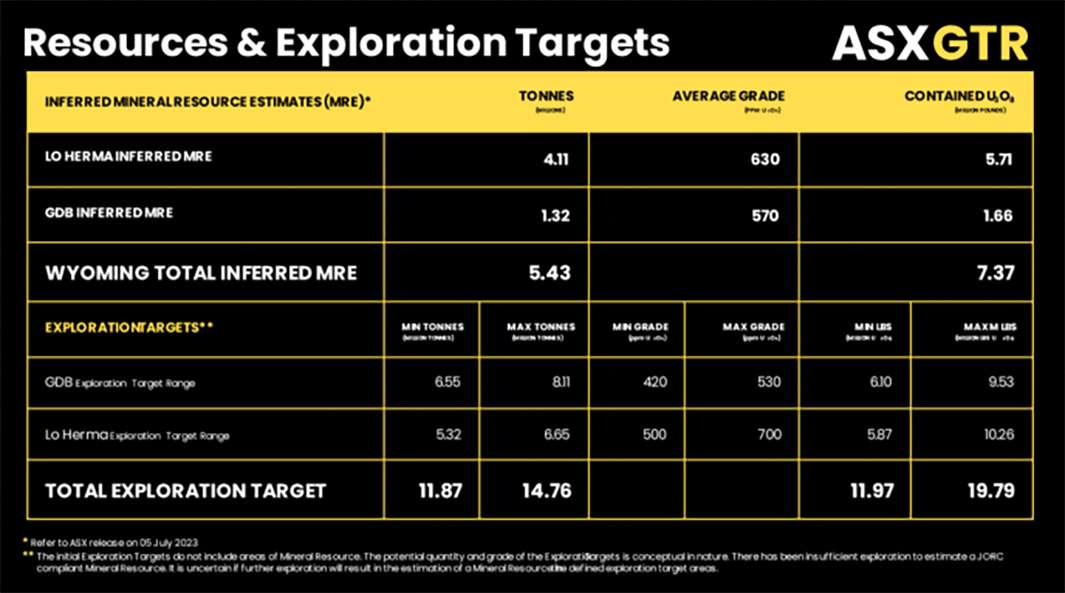

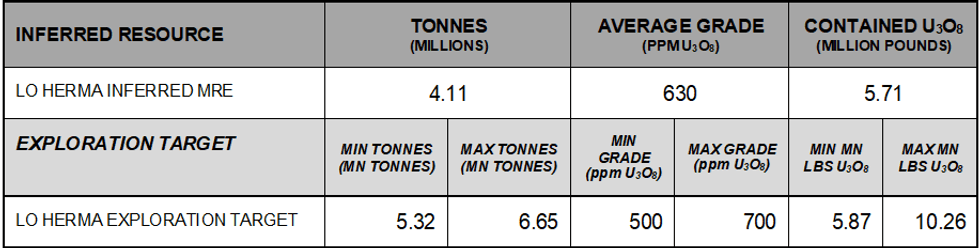

Maiden uranium resource and updated exploration target at the Lo Herma ISR project delivered an inferred mineral resource estimate of 5.71 Mlbs uranium oxide at an average 630 ppm plus an exploration target of an additional 5.87 to 10.26 Mlbs potential at average grade of 500 to 700 ppm.

Updated total resources across its Wyoming projects of 7.37 Mlbs plus an exploration target of an additional 11.97 to 19.79 Mlbs potential at average grade of 500 – 700 ppm.

In early 2022, the company completed a further 103 mud rotary exploration drill holes to increase the total trend length for GTI’s projects in the Great Divide Basin to 7.5 miles.

In late 2023, GTI completed 26 holes at Lo Herma to verify the historical data base & confirm exploration potential along trend & at depth.

GTI acquired a 1,771 drill hole data set over Lo Herma with a replacement value of AU$15 million.

GTI received its carbon neutral certification for its Australian head office and US field operations, through the Australian Government’s Climate Active Program.

GTI aims to utilize ISR mining at its Wyoming projects, which offers lower environmental impact, lower opex and capex than conventional mining.

GTI Energy has a highly experienced exploration team including the recent appointment of ISR specialist, Matt Hartmann, with a history of successful uranium discovery in Wyoming.

Key Projects

Wyoming Projects

The Wyoming projects are located in the Powder River & Great Divide Basins in Wyoming and the Henry Mountains (Colorado Plateau) Utah, United States. The Greta Divide Basin projects consist of the Thor, Logray, Loki, Odin, Teebo, Wicket and Green Mountain claims. The approximately 13,000 hectare group of projects is prospective for ISR-amenable sandstone-hosted roll-front uranium. The Wyoming projects are situated 5 to 30 kilometers from Ur-Energy’s Lost Creek ISR plant. The projects are also located near Rio Tinto’s Sweetwater/Kennecott Mill.

GTI Energy’s land holding in the Great Divide Basin was bolstered by the acquisition of the Green Mountain project comprising 5,585 hectares of contiguous ISR uranium exploration claims which abuts the Rio Tinto claims at Green Mountain. Historical drill data and geophysics confirms the presence of major uranium mineralisation at the projects.

Initial drilling at Lo Herma commenced in November 2023 and was completed in December with 26 drill holes successfully verifying the historical Lo Herma drill hole database. A drilling permit amendment is currently in progress aiming to optimise follow-up drilling, increase the total number of drill holes, and construct monitoring wells for groundwater data collection. Drilling is expected to resume by July 2024 with an enlarged program, and the mineral resource estimate and exploration targets are expected to be updated in the fourth quarter of 2024.

The company began initial exploration on Thor in 2021, and in 2022, it completed an additional 103 mud rotary exploration drill holes. The drilling of 70 holes was previously reported at the Thor prospect and an additional 33 holes combined have now been completed at the Odin, Teebo and Loki prospects. These 33 holes have discovered an additional combined 4.26 kilometers of ISR amenable uranium mineralised roll front trends increasing the total trend length for GTI’s projects in the Basin to 12.07 kilometers.

In February 2023, GTI Energy secured, by staking, approximately 3,500 hectares of unpatented mineral lode claims known as the Lo Herma project, about 16 kilometers from Cameco’s Smith Ranch-Highland ISR Uranium facility and Energy Fuels Nichols Ranch ISR plant. Lo Herma also lies within 97 kilometers of the companies leading the restart of uranium production in the USA, including Uranium Energy, Ur-Energy, Energy Fuels, Encore Energy and Peninsula Energy.

The company subsequently, secured a material historical data package for the project, which allowed GTI Energy to report a maiden uranium resource and exploration target update at the Lo Herma ISR project, including a cut-off grade of 200 parts per million (ppm) uranium oxide and a minimum grade thickness (GT) of 0.2 per mineralised horizon as 4.12 million tonnes of mineralisation at an average grade of 630 ppm uranium oxide for 5.71 million pounds (Mlbs) of uranium oxide contained metal. The inferred mineral resource estimate is 5.71 Mlbs uranium oxide at an average of 630 ppm.

The company also completed collection of aerial geophysical data at its Lo Herma, Green Mountain and Loki West ISR uranium exploration projects in Wyoming. The survey was conducted using a twin-engine aircraft loaded with a suite of sensors that provide detailed radiometric, magnetic and electromagnetic data, allowing for correlation between the three products.

The airborne geophysical survey at its Green Mountain project consequently updated its drill plan with 16 potential drill holes. The permit application process is underway for the 2024 drill program which aims to test the validity of the historical Kerr McGee drill hole maps, as well as the interpreted mineralised regions as determined from the airborne geophysical survey.

Henry Mountains Uranium Project

GTI’s uranium/vanadium projects in Utah are considered suitable for conventional mining and are located on the east flank of the Henry Mountains, covering 3,860 acres. The permits host historical production, open underground workings and have an exploration permit in place. The projects saw significant work from 2019 to 2021 including two drill programs totaling 52 drill holes and geophysical logging of an additional 76 historical drill holes. GTI subsequently elected to prioritise work at its newly acquired Wyoming ISR projects until such time as activity and investment in the region improves. The company’s projects lie within ~100 miles of Energy Fuels’ (NYSE American: UUUU) (TSX: EFR) White Mesa Mill and within a few miles of Anfield Energy’s (TSX.V: AEC) Shootaring (Ticaboo) mill site. The owners of both of these mills are actively pursuing mill re-starts.

In addition, Western Uranium & Vanadium (CSE:WUC) (OTCQX:WSTRF) has announced the purchase of a mill site in Green River Utah and work to design and permit the facility for processing uranium and vanadium. The plant, which will be located ~80 miles from GTI’s projects, is intended to process feed from Western's recently restarted Sunday Mine Complex over 160 miles away. Western advised of a mine operations restart at Sunday in February 2024. Western stated its new "mineral processing plant" will recover uranium, vanadium and cobalt from ore from Western's mines and that produced by other miners. Western said, on February 13, 2024, it expects the plant to be licensed and constructed for annual production of 1 million pounds U3O8 and 6 million pounds of V2O5, with initial production in 2025.

Based on the renewed interest in exploration, mining, and processing of uranium ore in this region, GTI is currently evaluating potential paths for further exploration, resource development, or other value creating activities with its Utah projects.

Management Team

Nathan Lude - Non-executive Chairman

Nathan Lude has broad experience working in the asset and fund management, mining, and energy industries. Lude is the founding director of Advantage Management, a corporate advisory firm. Lude has previously held directorships with ASX-listed mining companies.

Currently, he is the executive director of ASX-listed Hartshead Resources (ASX:ANA). Lude has grown a large business network across Australia and Asia, establishing strong ties with Australian broking firms, institutions, and Asian investors.

Bruce Lane - Executive Director

Bruce Lane has significant experience with ASX-listed and large industrial companies. Lane has held management positions in many global blue-chip companies as well as resource companies and startups in New Zealand, Europe and Australia. He holds a master’s degree from London Business School and is a graduate member of the Australian Institute of Company Directors. Lane has led a number of successful acquisitions, fund raising and exploration programs of uranium and other minerals projects during the last 15 years most notably with ASX listed companies Atom Energy Ltd & Stonehenge Metals Ltd & Fenix Resources Ltd (FEX).

James (Jim) Baughman - Executive Director

James Baughman is a highly experienced Wyoming uranium geologist and corporate executive who will help guide the company’s technical and commercial activities in the US. Baughman is the former president and CEO of High Plains Uranium (sold for US$55 million in 2006 to Uranium One) and Cyclone Uranium.

Baughman has more than 30 years of experience advancing minerals projects from grassroots to advanced stage. He has held senior positions (i.e., chief geologist, chairman, president, acting CFO, COO) in private and publicly traded mining & mineral exploration companies during his 30-year career.

He is a registered member of the Society of Mining, Metallurgy, Exploration and a member of the Society of Economic Geologists with a BSc in geology (1983 University of Wyoming) and is a registered professional geologist (P. Geo State of Wyoming). Baughman is a registered member of the Society of Mining, Metallurgy, and Exploration (SME) and a qualified person (QP) on the Toronto Stock Exchange (TSX) and Australian Stock Exchange (ASX).

Petar Tomasevic - Non-executive Director

Petar Tomasevic is the managing director of Vert Capital, a financial services company specializing in mineral acquisition and asset implementation. He has worked with several ASX-listed companies in marketing and investor relations roles. Tomasevic is fluent in five languages. He is currently appointed as a French and Balkans language specialist to assist in project evaluation for ASX-listed junior explorers. Most recently, he was a director at Fenix Resources (ASX:FEX), which is now moving into the production phase. He was involved in the company’s restructuring when it was known as Emergent Resources. Tomasevic was also involved in the company’s Iron Ridge asset acquisition, the RTO financing, and the development phase of Fenix’s Iron Ridge project.

Matt Hartmann - President of US Operations

Matt Hartmann is an executive and technical leader with more than 20 years of international experience and substantial uranium exploration and project development experience. He first entered into the uranium mining space in 2005 and followed a career path that has included senior technical roles with Strathmore Minerals and Uranium Resources. He is also a former principal consultant at SRK Consulting where he provided advisory services to explorers, producers and prospective uranium investors. Hartmann’s ISR uranium experience has brought him through the entire cycle of the business, from exploration, project studies and development, to production and well field reclamation. He has provided technical and managerial expertise to a large number of uranium ISR projects across the US including, Smith Ranch – Highland ISR Uranium Mine (Cameco), Rosita ISR Uranium Central Processing Plant and Wellfield (currently held by enCore Energy), the Churchrock ISR Uranium project (currently held by Laramide Resources), and the Dewey-Burdock ISR Uranium project (currently held by enCore Energy).

Matthew Foy - Company Secretary

Matthew Foy is an active member of the WA State Governance Council of the Governance Institute Australia. Foy has more than 14 years of experience in facilitating ASX-listing rule compliance. His core competencies are in the secretarial, operational, and governance disciplines for publicly listed companies. Foy has a working knowledge of the Australian Securities and Investments Commission and Australia Stock Exchange reporting. He has document drafting skills that provide the basis for valuable contributions to the boards on which he serves.

GTI Energy Ltd (ASX: GTR) (GTI or Company) is pleased to advise that planning for the 2024 field season in Wyoming has progressed well and permitting is on track to facilitate drilling during Q3.

Highlights

Lo Herma drilling permit amendment in progress to optimise follow-up drilling, increase total number of drill holes, and construct monitoring wells for groundwater data collection – drilling is scheduled for Q3 2024

Lo Herma Mineral Resource Estimate & Exploration Target to be updated in Q4 2024

Green Mountain maiden drilling planned for 2024 with permitting underway

Utah uranium/vanadium projects under evaluation to determine potential paths for renewed exploration, resource development or other value creating activities

LO HERMA PROJECT: 2024 DRILLING PERMIT AMENDMENT

42 drill holes remain permitted and undrilled at Lo Herma, however a review of the drilling conducted during December 2023 has helped the Company to refine and expand the planned 2024 drilling program to include 71 drill hole locations and construction of up to 5 groundwater monitoring wells. This next phase of exploration at Lo Herma will be focused on expanding the resource areas and where possible, upgrading the current mineral resource classification. Collection of important data including, hydrogeologic parameters of the mineralised aquifers and collection of rock core samples for metallurgical testing will be also prioritised.

GTI intends to mobilise drilling rigs to Lo Herma as soon as the activity is fully permitted, and environmental clearances are finalised. At this time, GTI anticipates that drilling will commence at Lo Herma during July 2024.

Following completion of the 2024 drill program at Lo Herma, GTI intends to publish an updated mineral resource estimate and exploration target range for the project. The Company expects that the updated mineral resource estimate will support near-term development of a Scoping Study to demonstrate the economic potential of the project.

The most recent drill results from Lo Herma and a summary of the project geology can be found in the Company’s 20 December 2023 news release.

GREEN MOUNTAIN PROJECT: DRILLING PERMIT

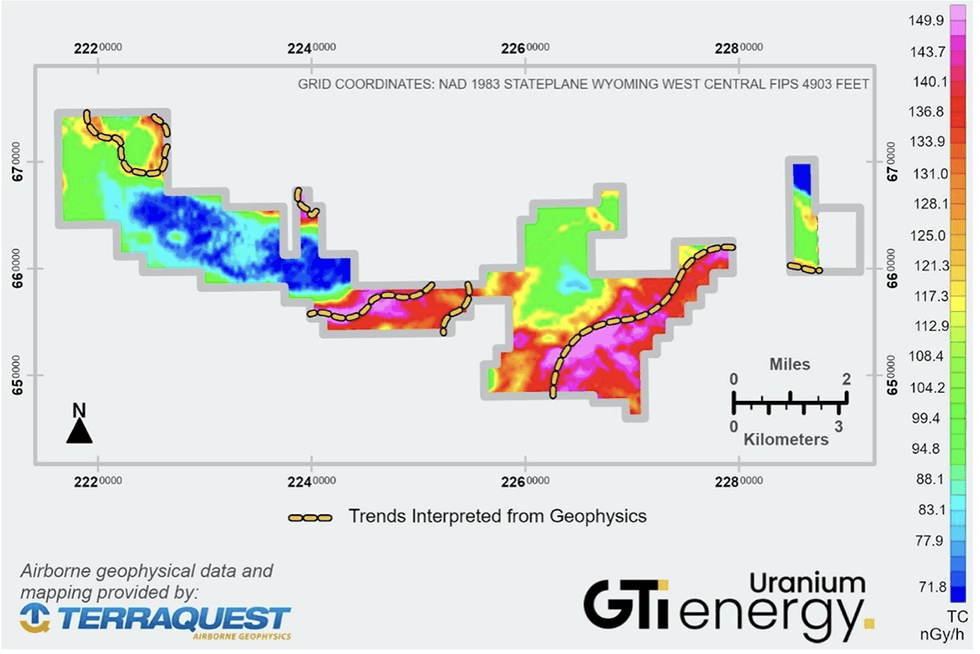

As previously advised on 21 November 2023, the Company completed an airborne geophysical survey at its Green Mountain Project to help refine a previously planned (but not permitted) drilling program. The now updated drilling plan includes 16 potential drill holes targeting 12 Miles of anomalous radiometric signature (Figure 1) which has been correlated with historical Kerr McGee drill holes maps.

A conceptual universe of 50 drill holes was initially developed with specific drill hole locations and access routes selected in consideration of site-specific topography and environmental considerations – the GTI technical team has now finalised this drill plan, selecting 16 drill holes that will be permitted for the 2024 drilling season should funding and weather conditions allow. The planned drill program will test the validity of the historical Kerr McGee drill hole maps, as well as the interpreted mineralised regions as determined from the airborne geophysical survey.

A “Class I Cultural Resource Report” and site Environmental Review have been completed with both of these studies incorporated into the planning of the drill program. Final on-site review of access will be completed as weather allows after which the Company will file the Drilling Notification. GTI will make a final decision to proceed once reclamation bonding is approved by Wyoming’s DEQ & the Federal BLM.

FIGURE 1. GREEN MOUNTAIN PROJECT SHOWS 12 MILES (19 KM) ANOMALOUS URANIUM TRENDS

GREEN MOUNTAIN PROJECT: GEOLOGIC SETTING AND MINERALISATION

The Green Mountain Project is located along the northeastern flank of the Great Divide Basin (GDB). The GDB consists of up to 25,000 feet of Mesozoic to Quaternary sediments and along with the Washaki Basin to the southwest, comprise the greater Green River Basin which occupies much of southwestern Wyoming. The Great Divide basin is structurally bounded by uplifted and fault displaced Precambrian rocks, creating an internally drained and isolated hydrogeologic basin.

This article includes content from GTI Energy, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.

GTI Energy Ltd (ASX: GTR) (GTI or Company) is pleased to report on its activities during the December quarter.

Initial 26-hole drilling program completed on time & on budget at Lo Herma

Results verified the historical Lo Herma drill hole database

Lo Herma exploration potential confirmed along trend in the Wasatch Formation and at depth in the Fort Union Formation

28 new claims staked at Lo Herma show promising exploration potential in the deeper Fort Union Formation which Cameco produces from ~10 miles east.

Positive results from airborne Magnetic & Radiometric Survey at Green Mountain

12 miles (19km) of anomalous uranium trends interpreted from airborne survey

6 prominent uranium anomalies identified across the Green Mountain Project

28 additional claims staked at Green Mountain, based on results of the geophysical surveys, bringing the total holdings to 697 claims for ~14,000 acres

Matt Hartmann appointed President US Operations with over 20 years of global mineral exploration, project development & commercial experience with significant track record in ISR uranium through the entire project life-cycle

Planning underway for 2024 expanded drill program at Lo Herma

LO HERMA ISR PROJECT EXPLORATION AND ADDITIONS TO LAND POSITION

During the quarter the Company advised that the initial drilling program had been completed at its 100% owned Lo Herma ISR Uranium Project (Lo Herma), located in Wyoming’s prolific Powder River Basin (Figures 1 & 2). Twenty-six (26) drillholes were advanced, totalling 4,250m (14,000 ft), with operations finalised on 11 December 2023 having been completed on time and on budget.

This initial drill program successfully validated the historical data package, used in preparing the Mineral Resource Estimate (MRE) for Lo Herma, through comparative analysis of stratigraphy & mineralised intercepts from new drill holes collocated with historical drill holes. Additional drill hole locations tested extensions of known mineralised trends and informed on redox conditions across several host sands to help refine and develop an expanded drill program planned at Lo Herma for 2024. These exploration holes confirmed the previously interpreted exploration potential at Lo Herma.

In addition, the Lo Herma land package was expanded through staking of 28 additional claims in December to cover extensions of interpreted trends as defined by the acquired historical data package. The historical data package includes several drill holes within the 28 new claims which contain mineralisation in a deeper Fort Union formation host sand. GTI is currently evaluating how the new claims and data impact the exploration target for the property and 2024 drill plans.

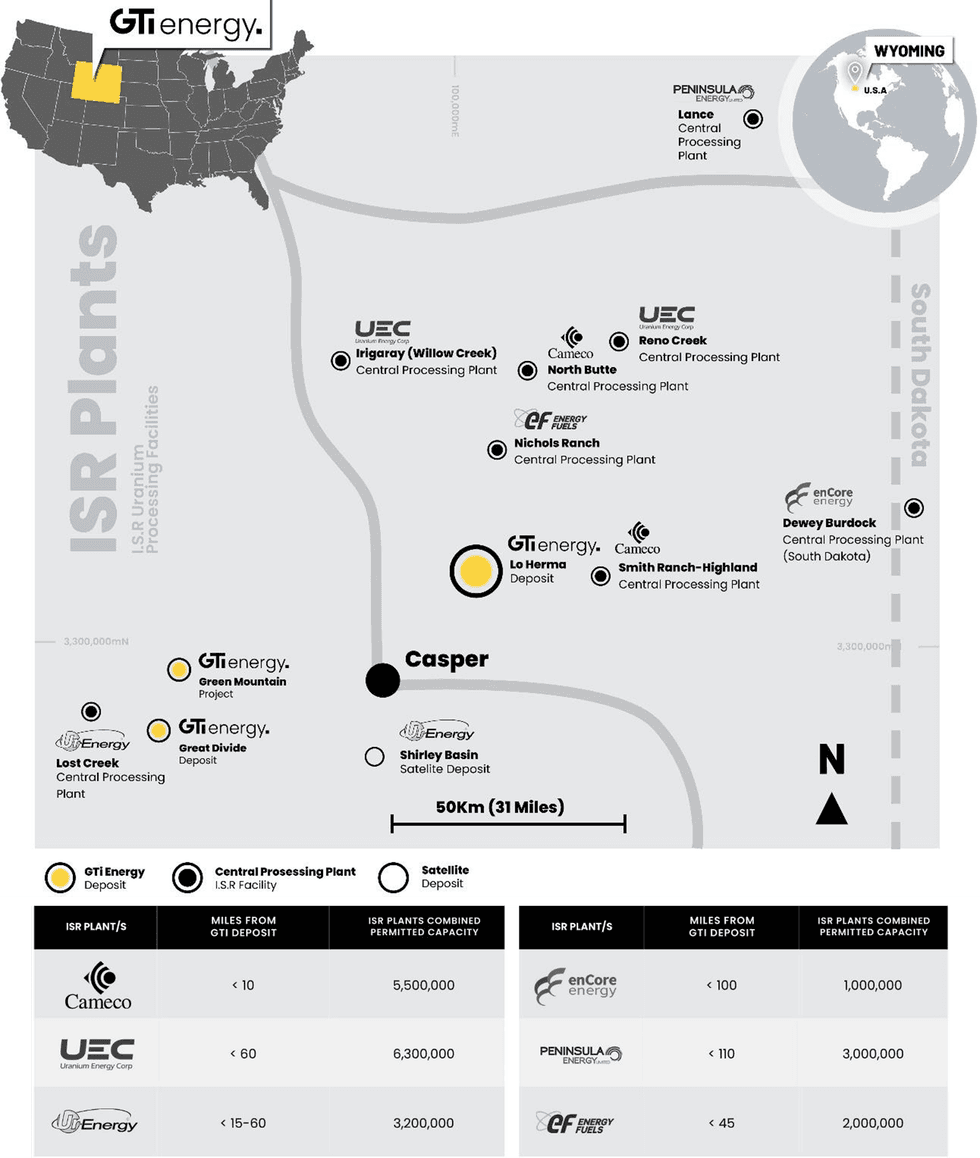

The Lo Herma ISR Uranium Project (Lo Herma) is located in Converse County, Powder River Basin (PRB), Wyoming (WY). The Project lies approximately 15 miles north of the town of Glenrock and within ~60 miles of five (5) permitted ISR uranium production facilities. Facilities include UEC’s Willow Creek (Irigaray & Christensen Ranch) & Reno Creek ISR plants, Cameco’s Smith Ranch-Highland ISR facilities & Energy Fuels Nichols Ranch ISR plant. The PRB has extensive ISR production history with numerous ISR uranium resources, central processing plants (CPP) & satellite deposits (Figure 1).

This article includes content from GTI Energy, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.

GTI Energy Ltd (ASX: GTR) (GTI or Company) is delighted to advise that experienced Denver based ISR uranium technical and executive leader, Mr Matt Hartmann has joined GTI in the role of President US Operations, to oversee the Company’s technical and commercial activities in the US.

Highlights

20+ years of global mineral exploration, project development & commercial experience, incl a significant track record in ISR uranium through the entire project life cycle

Uranium experience includes senior technical roles with Uranium Resources Inc. and Strathmore Minerals Corp, and industry consultant as a Principal with SRK. Most recently he was V.P. Technical Services for Sweetwater Royalties LLC, the largest private landowner in Wyoming

Previously provided technical & managerial expertise to several ISR uranium projects including, Cameco’s Smith Ranch–Highland, Encore’s Rosita central processing plant & wellfield, Laramide’s Churchrock and Encore’s Dewey-Burdock

Matt adds increased commercial & technical leadership of GTI’s interests in the US which will allow the company to more aggressively pursue its project development and commercialisation plans including strategic partnership opportunities

Matt Hartmann commented“I’m excited to be joining GTI to lead the company’s US operations. Activity in the uranium sector has increased significantly over the past year and the US is poised to return to meaningful uranium production in the near-term. GTI’s projects are extremely well located within 100 miles of 7 permitted ISR uranium facilities in Wyoming which is a very supportive state with a long history of uranium production. Over the past three years GTI has established itself in Wyoming and has assembled a portfolio of compelling uranium projects that would suggest the company is undervalued in the current US$100 per pound uranium market. I look forward to further developing GTI’s assets in the US & advancing the Lo Herma project towards a preliminary economic assessment.”

GTI Executive Director & CEO Bruce Lane commented“We are very pleased that Matt has agreed to join the team after having worked with us in the past. Matts skills and experience, particularly with ISR uranium in Wyoming, are a great fit for GTI as we look to accelerate the growth and development of our Wyoming ISR uranium resources. I have no doubt that Matt’s experience, skills and network in both the technical and commercial arenas will contribute very positively to our efforts to grow GTI into a significant US uranium company.”

MATT HARTMANN – EXPERIENCE SUMMARY

Mr. Hartmann is an executive and technical leader with 20+ years of international experience and substantial uranium exploration and project development experience. He first entered into the uranium mining space in 2005, and followed a career path that has included senior technical roles with Strathmore Minerals Corp. and Uranium Resources Inc. He is also a former Principal Consultant at SRK Consulting where he provided advisory services to explorers, producers & prospective uranium investors.

Mr. Hartmann’s ISR uranium experience has brought him through the entire cycle of the business, from exploration, project studies and development, through production and well field reclamation. He has provided technical and managerial expertise to a large number of uranium ISR projects across the US including, Smith Ranch – Highland ISR Uranium Mine (Cameco), Rosita ISR Uranium Central Processing Plant and Wellfield (currently held by enCore Energy), the Churchrock ISR Uranium Project (currently held by Laramide Resources), and the Dewey-Burdock ISR Uranium Project (currently held by enCore Energy).

This article includes content from GTI Energy, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.

GTI Energy Ltd (ASX: GTR) (GTI or Company) is pleased to advise that the initial drilling program has been completed at its 100% owned Lo Herma ISR Uranium Project (Lo Herma), located in Wyoming’s prolific Powder River Basin (Figures 1 & 2). Twenty-six (26) drillholes were advanced, totalling 4,250m (14,000 ft), with operations finalised on 11 December 2023.

Initial 26-hole drilling program completed on time & on budget at Lo Herma

Results have successfully verified the historical Lo Herma drill hole database

Exploration potential confirmed along trend in the Wasatch Formation and at depth in the Fort Union Formation

New claims staked at Lo Herma show promising exploration potential in the deeper Fort Union Formation which Cameco produces from ~10 miles east.

Planning in progress for expanded 2024 drill program targeting resource expansion, upgrade of current resource classification & hydrogeologic data collection

This initial drill program successfully validated the historical data package, used in preparing the Mineral Resource Estimate (MRE) for Lo Herma, through comparative analysis of stratigraphy & mineralised intercepts from new drill holes collocated with historical drill holes. Additional drill hole locations tested extensions of known mineralised trends and informed on redox conditions across several host sands to help refine and develop an expanded drill program planned at Lo Herma for 2024. These exploration holes confirmed the previously interpreted exploration potential at Lo Herma.

In addition, the Lo Herma land package was expanded through staking of 28 additional claims in December to cover extensions of interpreted trends as defined by the acquired historical data package. The historical data package includes several drill holes within the 28 new claims which contain mineralisation in a deeper Fort Union formation host sand. GTI is currently evaluating how the new claims and data impact the exploration target for the property and 2024 drill plans.

GTI Executive Director & CEO Bruce Lane commented“We are very pleased that initial drilling has successfully verified the large body of historical data used to prepare the Lo Herma JORC inferred resource. In addition, the drilling confirmed exploration potential along trend in the Wasatch formation and at depth in the Fort Union formation. The program was completed on time & budget with the data generated to be used to refine follow-up drilling in 2024. The drilling in 2024 is expected to upgrade the category of portions of the mineral resource & ultimately support a preliminary economic assessment for the project.”

LO HERMA URANIUM PROJECT – LOCATION & BACKGROUND

The Lo Herma ISR Uranium Project (Lo Herma) is located in Converse County, Powder River Basin (PRB), Wyoming (WY). The Project lies approximately 15 miles north of the town of Glenrock and close to seven (7) permitted ISR uranium production facilities. These facilities include UEC’s Willow Creek (Irigaray & Christensen Ranch) & Reno Creek ISR plants, Cameco’s Smith Ranch-Highland ISR facilities and Energy Fuels Nichols Ranch ISR plant (Figure 1). The Powder River Basin has extensive ISR uranium production history with numerous defined ISR uranium resources, central processing plants (CPP) & satellite deposits (Figure 1). The Powder River Basin has been the backbone of Wyoming U3O8 production since the 1970s.

As reported to ASX on 14 March 2023, a comprehensive historical data package, with an estimated replacement value of ~$15m, was purchased for the Lo Herma project in March of 2023. The data package includes original drill data for roughly 1,771 drill holes, from the 1970’s and 1980’s, pertaining to the Lo Herma region.

A total of 1,391 original drill hole logs were digitised for gamma count per second (CPS) data and converted to eU3O8% grades. 833 of these drill holes were located on GTI’s land position & used to prepare the MRE. 21 additional drill holes are located in the newly claimed area in Section 4 of Township 36N, Range 75W. Along with the 26 drill holes completed in this initial program, GTI now holds data from 880 drill holes within the current Lo Herma mineral holdings.

An initial Exploration Target for the Lo Herma project was previously announced to the ASX on 4 April 2023. An additional data package containing previously unavailable drill maps with geologically interpreted redox trends was subsequently secured by GTI as announced to the ASX on 27 June 2023 (refer to Table 1). Additional redox trends can now be interpolated based on the recent drilling and acquisition of the newly located mineral claims, however the Exploration Target has not been updated. GTI plans to update the mineral resource and exploration target estimates following execution of planned & permitted drilling during 2024.

TABLE 1: SUMMARY OF LO HERMA INFERRED MRE & EXPLORATION TARGETSThe potential quantity and grade of the Exploration Targets is conceptual in nature and there has been insufficient exploration to estimate a JORC-compliant Mineral Resource Estimate. It is uncertain if further exploration will result in the estimation of a Mineral Resource in the defined exploration target areas.

DRILLING RESULTS

The initial drilling program was completed 11 December 2023, with 26 mud rotary drill holes totalling 4,250m (14,000 ft). The drill targets were designed for verification of the historical drilling data, to test extensions of the mineralised redox trends, and explore the stratigraphic and oxidation conditions of the host sands in underexplored portions of the Lo Herma property.

Of 26 holes drilled, 6 holes met the minimum grade cutoff of 200 ppm eU3O8 & the total hole grade-thickness (GT) target of minimum 0.2 GT. Two drill holes met the minimum grade cutoff, but not the minimum GT. Fourteen (14) drill holes demonstrated trace mineralization but did not meet the grade cutoff. Four (4) drill holes were barren of any indication of mineralization. The best mineralized intercept was encountered in hole LH-23-006, with 19.0 feet with an average of 390 ppm eU3O8 for a total intercept grade-thickness of 0.741. The highest-grade intercept was encountered in hole LH-23-025, with 3.5 feet with an average of 800 ppm eU3O8, containing an internal 0.5 ft (~15 cm) interval of 1,890 ppm eU3O8.

Uranium assay values were obtained by probing the drill holes with a wireline geophysical sonde which includes a calibrated gamma detector, spontaneous potential, resistivity, and downhole drift detectors. The gamma detector senses natural gamma radiation emanations from the rock formations intercepted by the drill hole. The gamma levels are recorded on the geophysical logs. Using calibration, correction, and conversion factors, the measured gamma radiation is converted to an equivalent uranium ore grade (eU3O8) and compiled into uranium intercepts based on a minimum cutoff grade of 200 ppm eU3O8 in half-foot intervals. This is the industry standard method for uranium exploration in the US and is discussed in further detail in the JORC tables. The reader is cautioned that the reported uranium grades may not reflect actual uranium concentrations due to the potential for disequilibrium between uranium and its gamma emitting daughter products.

This article includes content from GTI Energy, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.

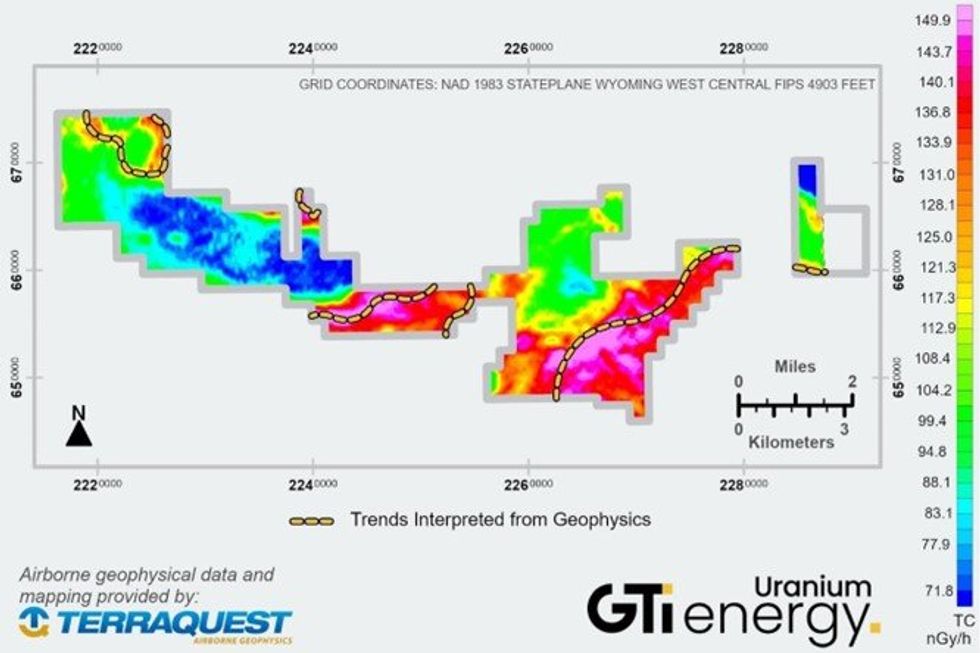

GTI Energy Ltd (ASX: GTR) (GTI or Company) is pleased to advise of positive results from the recently completed airborne radiometric and magnetic survey completed at its 100% owned Green Mountain Project (Project) located in Wyoming’s prolific Crooks Gap/Green Mountain/Great Divide Basin uranium production district.

Positive results from recent airborne Magnetic & Radiometric Survey

12 miles (19km) of anomalous uranium trends interpreted from airborne survey

6 prominent uranium anomalies were identified across the Project

Anomalies correlate with historically identified drill holes, interpreted trends, areas of past mining and/or known mineralisation

28 additional claims staked, based on results of the geophysical surveys, bringing the total holdings to 697 mining claims comprising circa 14,000 acres

Next steps: Planning & permitting for follow up drilling

GTI Executive Director Bruce Lane commented“The aerial geophysical survey has provided us with clear direction as to where to drill at Green Mountain. We have been able to utilise the historical drilling and geological information completed by Kerr McGee Corporation, Wold Nuclear and others during the 1970’s and 1980’s to help interpret and extrapolate significant additional anomalous uranium trends, particularly within the eastern part of the extensive Green Mountain land position. The land package is surrounded by significant uranium deposits and resources owned by Rio Tinto, Energy Fuels, Ur Energy & UEC, so we know we are in an area with real potential. Our next step is to progress work on refining drill targets and permitting”.

GTI’s 100% owned Green Mountain ISR Uranium Project (Green Mountain) is located in Sweetwater County, Great Divide Basin (GDB), Wyoming (WY) within a few miles of GTI’s Great Divide Basin projects and within 60 miles of GTI’s Lo Herma project in Wyoming’s Powder River Basin (Figure 1).

GTI’s Green Mountain Project covers ~14,000 acres (~5,665 hectares) of underexplored mineral lode claims (Claims) and benefits from historical Kerr McGee uranium drilling data and oil-well exploration drill logs which confirm the presence of roll fronts within the Battle Springs formation which hosts neighbouring major uranium deposits.

The Properties are located in the neighbourhood of Energy Fuel’s (EFR) 30Mlb Sheep Mountain deposit, Ur-Energy’s (URE) 14Mlb Lost Soldier ISR deposit, UEC’s (UEC) Antelope deposit & Rio Tinto’s (RIO) Big Eagle (past producing), Jackpot, Desert View, Phase II, & Willow Creek deposits (Figure 2). The Claims lie south of Green Mountain, ~5kms from GTI’s existing Odin claim group & within 15km of GTI’s Thor project where two successful drill programs were completed during 2022.

This article includes content from GTI Energy, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.

“We don't need any more catalysts. We've got a 30 million to 50 million pound supply deficit in the market probably for the next five years. That's what we're looking at. And that's what's going to move the price" — Justin Huhn, Uranium Insider

"To us (nuclear energy) was always the answer. And while everyone seems very pessimistic about everything, I think that perhaps we could be on the verge of a huge, major transformation where finally we do appreciate nuclear for the unbelievable technology that it is." — Adam Rozencwajg, Goehring & Rozencwajg

Who We Are

The Investing News Network is a growing network of authoritative publications delivering independent,

unbiased news and education for investors. We deliver knowledgeable, carefully curated coverage of a variety

of markets including gold, cannabis, biotech and many others. This means you read nothing but the best from

the entire world of investing advice, and never have to waste your valuable time doing hours, days or weeks

of research yourself.

At the same time, not a single word of the content we choose for you is paid for by any company or

investment advisor: We choose our content based solely on its informational and educational value to you,

the investor.

So if you are looking for a way to diversify your portfolio amidst political and financial instability, this

is the place to start. Right now.

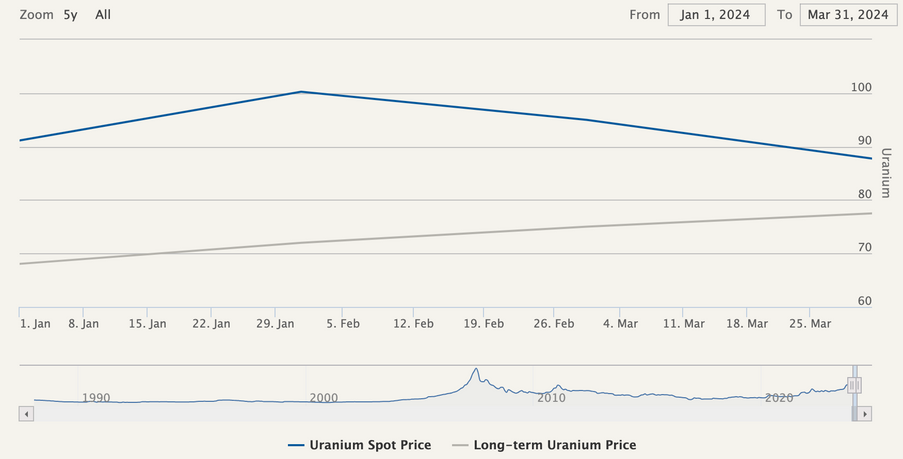

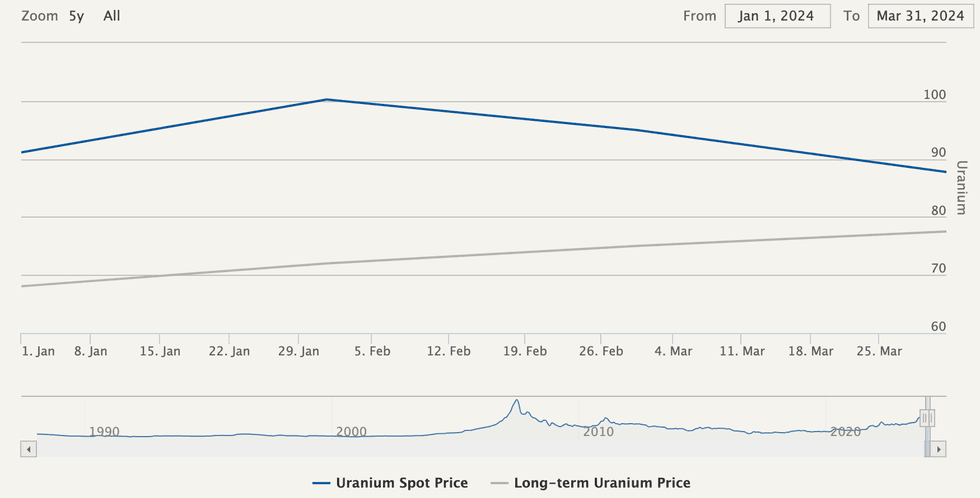

The uranium spot price displayed volatility in Q1, rising to a high unseen since 2007 before ending the quarter below US$90 per pound. U3O8 values shed 3.96 percent over the three month period, but experts believe fundamentals remain strong and expect the sector to benefit from various tailwinds in the months ahead.

Supply remains a key factor in the uranium landscape, with a deficit projected to grow amid production challenges. With annual output well below the current demand levels, the supply crunch is expected to be a long-term price driver.

“Supply-side fragility continued to be one of the key themes in Q1, especially the news out of Kazakhstan that production would be significantly lower than expected in 2024 than previously thought,” Ben Finegold, associate at London-based investment firm Ocean Wall, told the Investing News Network in an interview.

These favorable fundamentals are expected to support uranium prices for the remainder of the year.

Finegold also noted that spot market activity highlights how sensitive the sector is to supply challenges.

“Spot market prices have also been a key talking point as volatility in pricing has increased dramatically in Q1 to both the upside and downside,” he explained. “It has brought to light just how thinly traded the spot market is, but interestingly term prices have only continued to rise, which is indicative that the long-term fundamentals remain intact.”

Sulfuric acid shortage impeding supply growth

The U3O8 spot price opened the year at US$91.71 and edged higher through January 22, when values hit a 17 year high of US$106.87. However, the near two decade record was short lived, and by month’s end uranium was around US$100.

Some of the price positivity early in the quarter came as Kazatomprom (LSE:KAP,OTC Pink:NATKY) warned that it was expecting to adjust its 2024 production guidance due to “challenges related to the availability of sulfuric acid.”

The state producer and major uranium player confirmed the reduction on February 1, underscoring the importance of sulfuric acid in its in-situ recovery method and describing its efforts to secure supply.

“Presently, the company is actively pursuing alternative sources for sulfuric acid procurement,” a press release states.

“Looking ahead in the medium term, the deficit is expected to alleviate as a result of the potential increase in sulphuric acid supply from local non-ferrous metals mining and smelting operations. The company also intends to enhance its in-house sulfuric acid production capacity by constructing a new plant.”

In 2023, Kazatomprom initiated the establishment of Taiqonyr Qyshqyl Zauyty to oversee the construction of a new sulfuric acid plant capable of producing 800,000 metric tons annually.

In the years ahead, the company is aiming to bolster its sulfuric acid production capacities through existing partnerships to achieve a consolidated production volume of approximately 1.5 million metric tons.

In the meantime, disruptions to Kazakh output will only grow the market deficit.

According to the World Nuclear Association, total global uranium production in 2022 only satiated 74 percent of global demand, a number that is likely to shrink as nuclear reactors in Asian countries begin coming online.

“Kazakhstan is the largest producer of uranium in the world — 44 percent. We like to think of Kazakhstan as the OPEC of uranium,” John Ciampaglia, CEO of Sprott Asset Management, said during a recent webinar.

Kazatomprom forecasts its adjusted uranium production for 2024 will range between 21,000 and 22,500 metric tons on a 100 percent basis, and 10,900 to 11,900 metric tons on an attributable basis. While in line with the company’s 2023 output, the major had to forgo a production ramp up due to the sulfuric acid shortage and development issues.

Analysts and market watchers foresee the sulfuric acid shortage being a long-term price driver.

“The sulfuric acid issue in Kazakhstan is a systemic problem that we do not believe will go away any time soon,” said Finegold. “While the company is doing what they can to alleviate pressures on sulfuric acid supplies, we believe their ability to ramp up production will be hindered for several years before their third domestic plant comes online. As such, we do not see Kazakh uranium production increasing significantly over the next three to four years.”

COP28 nuclear commitment supporting demand

The U3O8 spot price spiked again in early February, reaching US$105 before another correction set in.

As Finegold explained, some of the retraction was the result of profit taking from short-term holders.

“Financial speculators looking to lock in profits towards March year ends played a role, but as we know these moves are achieved on very little volume, so the point remains that the long-term thesis remains unchanged,” he said.

Finegold went on to highlight the different investment perspectives within the market.

“Spot market participants trade on very different parameters and time horizons to one another,” he said. “A trader and a hedge fund, for example, act in a totally different manner to a utility who are long-term thinkers.”

Despite February's slight contraction, uranium prices have remained elevated above US$80.

Some of this long-term support is the result of a COP28 nuclear capacity declaration. At the organization's December meeting in Dubai, more than 20 countries signed a proclamation to triple nuclear capacity by 2050.

There are currently 440 operational nuclear reactors with an additional 13 slated to come online this year and another 47 expected to start electricity generation by 2030. For Finegold, this commitment to building and fortifying nuclear capacity has been uranium's most prevalent demand trend. “The demand side of the equation remains robust and growing at a time when the supply side has never been more fragile,” he commented.

Others also believe the COP28 commitment was a tipping point for the uranium market that spawned several announcements about mine restarts and project extensions.

“Governments around the world have acknowledged that they need to be more supportive, not just financially, but in terms of expediting new projects, expediting the environmental permitting processes for new uranium mines,” said Sprott’s Ciampaglia during the webinar. “And it's not just happening in one country — with the exception of one or two outliers in Europe, this is happening around the globe.”

Geopolitical risk and resource nationalism are price catalysts

Uranium prices continued to consolidate from mid-February through mid-March, but remained above US$84.

This positivity saw several uranium companies in the US, Canada and Australia announce plans to bring existing mines out of care and maintenance. In late November, uranium major Cameco (TSX:CCO,NYSE:CCJ) announced it was restarting operations at its McArthur River/Key Lake project in Saskatchewan after four years.

In January, the McClean Lake joint venture which is co-owned by Denison Mines (TSX:DML,NYSEAMERICAN:DNN) and Orano Canada, reported plans to restart its McClean Lake project, also located in the Athabasca Basin of Saskatchewan.

South of the border, exploration company IsoEnergy (TSXV:ISO,OTCQX:ISENF) is gearing up to restart mining at its Tony M underground mine in Utah. “With the uranium spot price now trading around US$100 per pound, we are in the very fortunate position of owning multiple, past-producing, fully permitted uranium mines in the U.S. that we believe can be restarted quickly with relatively low capital costs," IsoEnergy CEO and Director Phil Williams said in a February release.

Building North American capacity is especially important ahead of the global nuclear energy ramp up and the ongoing geopolitical tensions between Russia and the west. While nuclear power is used to provide nearly 20 percent of America's electricity, the nation produces a very small amount of the uranium it needs.

Instead, the country imports as much as 40.5 million pounds annually.

According to the US Energy Information Administration, 27 percent of imports come from ally nation Canada, while 25 percent of imports come from Kazakhstan and 11 percent originate in Uzbekistan — both considered allies of Russia.

Commenting on that topic, Finegold noted, “The ongoing talk around US sanctions remains the most significant geopolitical catalyst for the sector." He added, "While we do not believe sanctions could be enforced immediately, it will send a signal to the market that Russia will no longer be involved in the largest uranium market in the world and would inevitably have an impact on fuel cycle component prices.”

If sanctions do limit imports from Russian allies, Finegold expects these countries to form stronger ties to China.

“Outside of this, the relationship between Kazakhstan and China remains one to watch as the Chinese continue their nuclear rollout strategy and look to procure millions of Kazakh-produced pounds,” he added.

Uranium price outlook remains positive

After hitting a Q1 low of US$84.84 on March 18, uranium began to move positively, ending the three month session in the US$88 range. Commitments to nuclear capacity, the energy transition and stifled supply will continue to be the most prevalent market drivers heading into the second quarter and the rest of the year.

“We believe uranium prices will significantly outrun the recent US$107 highs from February in 2024, driven by a fundamental supply/demand imbalance,” said Finegold. “Producers will continue to cover production shortfalls, while utilities struggle to replenish inventory shortages.”

The Ocean Wall associate went on to note, “The inherent appetite of traders and financial speculators will continue to drive prices higher. These demand drivers are converging at a time when supply has never looked more fragile.”

Don’t forget to follow us @INN_Resource for real-time updates!

Securities Disclosure: I, Georgia Williams, hold no direct investment interest in any company mentioned in this article.

Editorial Disclosure: The Investing News Network does not guarantee the accuracy or thoroughness of the information reported in the interviews it conducts. The opinions expressed in these interviews do not reflect the opinions of the Investing News Network and do not constitute investment advice. All readers are encouraged to perform their own due diligence.

Justin Huhn: Uranium Price, Supply and Stocks in 2024 — Plus Cameco Analysis

All eyes were on uranium at the end of 2023 as the energy fuel soared through US$100 per pound.

But where is the market headed this year? Justin Huhn, founder and publisher of Uranium Insider, shared his thoughts in an extensive interview with the Investing News Network, emphasizing his continued bullishness.

Outlining current supply/demand dynamics, Huhn said that although 2023's sizeable deficit of about 40 million pounds will shrink a little in 2024, he sees a "very large" deficit persisting for a number of years.

Huhn sees this situation pushing prices for uranium much higher, although he didn't give an exact number.

"The price isn't going to make sense for anybody," he said. "We can arguably go up another US$20 — that will arguably incentivize every project in the world to be profitable. But the price is going to go far beyond that simply driven by the substantially larger amount of demand than we have for supply."

In terms of which stocks to focus on, Huhn said since December small- and mid-cap companies have been outperforming larger-cap companies — he's tracking that movement via the Sprott Junior Uranium Miners ETF (NASDAQ:URNJ), which holds a basket of small- and mid-cap uranium stocks, and sector major Cameco (TSX:CCO,NYSE:CCJ).

"The main theory around this is that as the story gets more popular due to its relative performance and it starts to attract more investment attention, you're going to attract more retail investors, and the retail investors largely go after the smaller companies because they believe that there's torque in those companies. And there is torque in those smaller companies," he explained during the conversation. "Unfortunately, when risk is off, that torque is to the downside. When it's on they can outperform by orders of magnitude."

Watch the interview above for Huhn's full thoughts on the topics discussed above, as well his analysis of Cameco's latest results, contracting in the uranium space and why the sector doesn't need any more catalysts.

Don't forget to follow us @INN_Resource for real-time updates!

Securities Disclosure: I, Charlotte McLeod, hold no direct investment interest in any company mentioned in this article.

Editorial Disclosure: The Investing News Network does not guarantee the accuracy or thoroughness of the information reported in the interviews it conducts. The opinions expressed in these interviews do not reflect the opinions of the Investing News Network and do not constitute investment advice. All readers are encouraged to perform their own due diligence.

Lobo Tiggre: Uranium Back on the Table, When Will Gold Stocks Move?

Speaking to the Investing News Network, Lobo Tiggre, CEO of IndependentSpeculator.com, shared his thoughts on uranium's recent price pullback and gold's new nominal all-time high.

"I'm putting uranium back on the table again. I'm actually as bullish again now on uranium as I am on gold for this year. I think both are going to do really well," he said at the Prospectors & Developers Association of Canada (PDAC) convention.

Watch the interview for more from Tiggre on uranium and gold. You can also click here for our PDAC playlist.

Don't forget to follow us @INN_Resource for real-time updates!

Securities Disclosure: I, Charlotte McLeod, hold no direct investment interest in any company mentioned in this article.

Editorial Disclosure: The Investing News Network does not guarantee the accuracy or thoroughness of the information reported in the interviews it conducts. The opinions expressed in these interviews do not reflect the opinions of the Investing News Network and do not constitute investment advice. All readers are encouraged to perform their own due diligence.

Affiliate Disclosure: The Investing News Network may earn commission from qualifying purchases or actions made through the links or advertisements on this page.

Gwen Preston: Gold Gearing Up for Next Move, Safest Bets in Uranium

Speaking to the Investing News Network, Gwen Preston of Resource Maven shared her thoughts on gold in 2024, noting that the yellow metal should work for investors from the middle of the year onward.

"I think the next move up in gold is going to require the rate cut — we've had the expectation of the rate cut built into the price, that's why we've gone up to new highs," she said at the Vancouver Resource Investment Conference (VRIC). "But we're still really in that sideways trend ... I think actually breaking through it will require the rate cut."

Looking over to uranium, Preston said that although the price has moved substantially in recent months, the commodity's supply/demand dynamics are such that it could "easily" jump to US$140 per pound overnight.

In terms of supply, uranium has become a seller's market. While companies are working to bring new mines online and restart idled production, the process won't be quick. She sees some relief coming from hedge funds that bought uranium at low prices and are now ready to sell, but emphasized that the volumes they'll be able to provide will be small.

There's also the east/west divide in the sector. Preston noted that the US Senate is likely to approve a ban on Russian uranium imports — and if that happens, Russia will probably preemptively cut off sales of the material to the US.

"There just isn't supply ... despite a few little setbacks that maybe create a trading range for a little while here to stabilize this huge price run that we've seen, I think (the price) will still go higher. I'm very confident that the price is going to end 2024 higher than the insane price that it began the year at. Because it's not actually insane. It's a valid representation of the lack of this essential commodity that the utilities need," she explained during the conversation.

In Preston's view, the safest uranium stocks right now are those with growing US production — those include Uranium Energy (NYSEAMERICAN:UEC), enCore Energy (TSXV:EU,NASDAQ:EU) and Energy Fuels (TSX:EFR,NYSEAMERICAN:UUUU).

Watch the interview above for more from Preston on gold and uranium. You can also click here for the Investing News Network's full VRIC playlist on YouTube.

Don't forget to follow us @INN_Resource for real-time updates!

Securities Disclosure: I, Charlotte McLeod, hold no direct investment interest in any company mentioned in this article.

Editorial Disclosure: Energy Fuels is a client of the Investing News Network. This article is not paid-for content.

The Investing News Network does not guarantee the accuracy or thoroughness of the information reported in the interviews it conducts. The opinions expressed in these interviews do not reflect the opinions of the Investing News Network and do not constitute investment advice. All readers are encouraged to perform their own due diligence.

The spot uranium price added 86.41 percent to its value in 2023 and started 2024 at US$90.98 per pound. By late January, prices for the energy commodity had rallied to a 17 year high of US$106.

However, as Q1 progressed, uranium saw some consolidation. By March 11, values had slipped below US$90 for the first time since late December. Even so, prices remain historically high, holding above US$85 as of April 10.

Uranium's sustained high values following years of underperformance underscore its positive supply and demand dynamics, which are improving as nuclear power becomes an important factor in the energy transition.

During an interview with the Investing News Network at the annual Prospectors & Developers Association of Canada convention in March, Scott Melbye of Uranium Energy (NYSEAMERICAN:UEC) and Uranium Royalty (TSX:URC,NASDAQ:UROY) expressed optimism about the current price trajectory for the energy fuel.

"There's nothing to keep uranium from going to US$150, US$200 in this environment," he said.

Below are the top uranium stocks on the TSX, TSXV and CSE by share price performance so far this year. All data was obtained on April 9, 2024, using TradingView’s stock screener, and all companies had market caps above C$10 million at the time. Read on to learn what factors have been moving their share prices.

District Metals is an energy metals and polymetallic explorer and developer with a portfolio of nine assets, including five uranium projects in Sweden. It's currently focused on its Viken property, which hosts a uranium-vanadium deposit.

Historic estimates conducted in 2010 and 2014 peg the indicated resource at 43 million metric tons with an average grade 0.019 percent U3O8, with another 3 billion metric tons with an average grade 0.017 percent U3O8 in the inferred category. According to the company, Viken is one of the “world's largest in terms of uranium and vanadium mineral resources."

Shares of District spiked to a Q1 high of C$0.37 on March 11, shortly after the Swedish government announced plans to review a nation-wide ban on uranium mining and exploration that has been in place since 2018.

“We are very pleased with this official statement from the Swedish Government and believe it is a significant step towards lifting the current uranium mining moratorium in Sweden,” Garrett Ainsworth, CEO of District, said. “The Swedish Government has made its intentions clear by stating that ‘the current ban on uranium mining will be removed.’ District is ready for this transformational decision with our portfolio of properties in Sweden.”

Earlier in the quarter, the company completed the acquisition of the remaining four mineral licenses at Viken.

Canada-focused Greenridge Exploration is currently engaged in the exploration of the Nut Lake uranium project in the Thelon Basin in Nunavut, Canada. The Nut Lake asset spans 4,036 hectares, and the company says it is strategically positioned near the Angilak uranium deposit, which was recently acquired by Atha Energy (TSXV:SASK,OTCQB:SASKF) through a three way merger with Latitude Uranium and 92 Energy.

Nut Lake is a new property for Greenridge — on January 18, the company entered into an option agreement with three parties to acquire a 100 percent stake in the asset. Historic drilling at the polymetallic deposit has identified “significant” uranium mineralization, with intersections of up to 9 feet containing 0.69 percent of U3O8.

On March 28, the uranium explorer announced the addition of Sean Hillacre to its advisory team. Hillacre, who is the president and vice president of exploration at Standard Uranium (TSXV:STND,OTCQB:STTDF), has more than 10 years of experience as a geologist in Saskatchewan's Athabasca Basin. Some of that time was spent on the technical team at NexGen Energy (TSX:NXE,NYSE:NXE,ASX:NXG) advancing the Arrow uranium deposit toward production.

Shares of Greenridge trended higher through Q1, reaching a high of C$0.78 for the period on March 31.

Exploration company Myriad Uranium holds a significant interest in two promising uranium projects. At Wyoming's Copper Mountain uranium project, in which it possesses a 75 percent earnable interest, the company is aiming to tap into the “world-class” potential of the district. The state is the US’ top producer of uranium.

Myriad also has an 80 percent stake in uranium exploration licenses comprising 1,800 square kilometers in Niger's Tim Mersoï Basin, another jurisdiction that boasts world-class uranium deposits.

Shares of Myriad registered a Q1 high early in the period, hitting C$0.39 on January 21. The share price bump coincided with news that the company was welcoming “renowned geologist and the pre-eminent authority on Copper Mountain and its uranium endowment” Jim Davis, to its technical committee.

Commenting on the appointment, Myriad CEO Thomas Lamb said, “On October 31, 2023, we announced historic resource estimates and resource targets relating to Copper Mountain. These estimates and targets were the product of C$100 million in exploration and development spends by Union Pacific during the 1970s. Much of this work was led by Jim Davis, and we are delighted he is joining our Technical Committee.”

CanAlaska Uranium is a self-described project generator with a portfolio of assets in the Athabasca Basin. The region is well known in the sector for its high-grade deposits, which helped birth the moniker "the Saudi Arabia of Uranium."

The company's five asset portfolio includes the West McArthur property, which is situated near sector major Cameco (TSX:CCO,NYSE:CCJ) and Orano Canada’s McArthur River mine. In 2018, Cameco signed on as a joint venture partner for CanAlaska's project and the company retains a 16.65 percent stake.

The uranium explorer made several announcements over the 90 day period, including the approval of a C$7.5 million exploration program at West McArthur. On February 28, the company reported high-grade intersections at the Pike zone at West McArthur. The discovery was made during the exploration firm's winter drill campaign.

The statement drill hole, WMA082-4, intersected 13.75 percent U3O8 equivalent (eU3O8) over 16.8 meters, including 40.3 percent eU3O8 over 4.7 meters and 13.54 percent eU3O8 over 2 meters. CanAlaska’s share price jumped from C$0.46 on February 27 to C$0.74 the day of the news, and marked a Q1 high of C$0.75 on March 7.

Premier American Uranium is focused on consolidating, exploring and developing uranium projects in the US. The company, which was spun out of Consolidated Uranium in late 2023, currently has four assets in two major uranium-producing jurisdictions: Wyoming's Great Divide Basin and Colorado's Uravan Mineral Belt.

On March 20, Premier announced plans to acquire American Future Fuel (OTCQB:AFFCF), which would give Premier access to the Cebolleta uranium project located within the Grants Mineral Belt of New Mexico.

The all-share deal will see the combined value of the merged companies sit at C$129 million.

“The announcement … marks a significant leap in our journey to strengthen our foothold in the US uranium market through opportunistic and strategic M&A,” said Tim Rotolo, chairman of Premier American Uranium. “By acquiring a key project, we’re not just enriching our portfolio; we’re also setting our roots in three principal uranium regions, paving the way for rapid growth.” Shares of Premier reached a quarterly high of C$3.09 on February 8.

Uranium is primarily used for the production of nuclear energy, a form of clean energy created in nuclear power plants. In fact, 99 percent of uranium is used for this purpose. As of 2022, there were 439 active nuclear reactors, as per the International Atomic Energy Agency. Last year, 8 percent of US power came from nuclear energy.

The commodity is also used in the defense industry as a component of nuclear weaponry, among other uses. However, there are safeguards in effect to keep this to a minimum. To create weapons-grade uranium, the material has to be enriched significantly — above 90 percent — to the point that to achieve just 5.6 kilograms of weapons-grade uranium, it would require 1 metric ton of uranium pre-enrichment.

Because of this necessity, uranium enrichment facilities are closely monitored under international agreements. Uranium used for nuclear power production only needs to be enriched to 5 percent; nuclear enrichment facilities need special licenses to enrich above that point for uses such as research at 20 percent enrichment.

The metal is also used in the medical field for applications such as transmission electron microscopy. Before uranium was discovered to be radioactive, it was used to impart a yellow color to ceramic glazes and glass.

Where is uranium found?

The country with the greatest uranium reserves by far is Australia — the island nation holds 28 percent of the world’s uranium reserves. Rounding out the top three are Kazakhstan with 15 percent and Canada with 9 percent.

Although Australia has the highest reserves, it holds uranium as a low priority and is only fourth overall for production. All its uranium output is exported, with none used for domestic nuclear energy production.

Kazakhstan is the world’s largest producer of the metal, with production of 21,227 metric tons in 2022. The country’s national uranium company, Kazatomprom, is the world’s largest producer.

Canada’s uranium reserves are found primarily in its Athabasca Basin, and the region is a top producer of the metal as well, although some of the major mines have been under care and maintenance in recent years.

Why should I buy uranium stocks?

Investors should always do their own due diligence when looking at any commodity so that they can decide whether it fits into their investment plans. With that being said, many experts are convinced that uranium has entered into a significant bull market, meaning that uranium stocks could be a good buy.

A slew of factors have led to this bull market. While the uranium industry spent the last decade or so in a downturn following the 2011 Fukushima nuclear disaster, discourse has been building around the metal's use as a source of clean energy, which is important for countries looking to reach climate goals. Nations are now prioritizing a mix of clean energies such as solar and wind energy alongside nuclear. Significantly, in August 2022, Japan announced it is looking into restarting its idled nuclear power plants and commissioning new ones.

Uranium prices are very important to uranium miners, as in recent years levels have not been high enough for production to be economic. However, in 2024, prices spiked from the US$58 in August 2023 to a high of US$106 per pound U3O8 in February 2024. At this price level, uranium stocks remain highly undervalued.

Don’t forget to follow us @INN_Resource for real-time updates!

Securities Disclosure: I, Georgia Williams, hold no direct investment interest in any company mentioned in this article.

The uranium spot price displayed volatility in Q1, rising to a high unseen since 2007 before ending the quarter below US$90 per pound. U3O8 values shed 3.96 percent over the three month period, but experts believe fundamentals remain strong and expect the sector to benefit from various tailwinds in the months ahead.

Supply remains a key factor in the uranium landscape, with a deficit projected to grow amid production challenges. With annual output well below the current demand levels, the supply crunch is expected to be a long-term price driver.

“Supply-side fragility continued to be one of the key themes in Q1, especially the news out of Kazakhstan that production would be significantly lower than expected in 2024 than previously thought,” Ben Finegold, associate at London-based investment firm Ocean Wall, told the Investing News Network in an interview.

These favorable fundamentals are expected to support uranium prices for the remainder of the year.

Finegold also noted that spot market activity highlights how sensitive the sector is to supply challenges.

“Spot market prices have also been a key talking point as volatility in pricing has increased dramatically in Q1 to both the upside and downside,” he explained. “It has brought to light just how thinly traded the spot market is, but interestingly term prices have only continued to rise, which is indicative that the long-term fundamentals remain intact.”

Sulfuric acid shortage impeding supply growth

The U3O8 spot price opened the year at US$91.71 and edged higher through January 22, when values hit a 17 year high of US$106.87. However, the near two decade record was short lived, and by month’s end uranium was around US$100.

Some of the price positivity early in the quarter came as Kazatomprom (LSE:KAP,OTC Pink:NATKY) warned that it was expecting to adjust its 2024 production guidance due to “challenges related to the availability of sulfuric acid.”

The state producer and major uranium player confirmed the reduction on February 1, underscoring the importance of sulfuric acid in its in-situ recovery method and describing its efforts to secure supply.

“Presently, the company is actively pursuing alternative sources for sulfuric acid procurement,” a press release states.

“Looking ahead in the medium term, the deficit is expected to alleviate as a result of the potential increase in sulphuric acid supply from local non-ferrous metals mining and smelting operations. The company also intends to enhance its in-house sulfuric acid production capacity by constructing a new plant.”

In 2023, Kazatomprom initiated the establishment of Taiqonyr Qyshqyl Zauyty to oversee the construction of a new sulfuric acid plant capable of producing 800,000 metric tons annually.

In the years ahead, the company is aiming to bolster its sulfuric acid production capacities through existing partnerships to achieve a consolidated production volume of approximately 1.5 million metric tons.

In the meantime, disruptions to Kazakh output will only grow the market deficit.

According to the World Nuclear Association, total global uranium production in 2022 only satiated 74 percent of global demand, a number that is likely to shrink as nuclear reactors in Asian countries begin coming online.

“Kazakhstan is the largest producer of uranium in the world — 44 percent. We like to think of Kazakhstan as the OPEC of uranium,” John Ciampaglia, CEO of Sprott Asset Management, said during a recent webinar.

Kazatomprom forecasts its adjusted uranium production for 2024 will range between 21,000 and 22,500 metric tons on a 100 percent basis, and 10,900 to 11,900 metric tons on an attributable basis. While in line with the company’s 2023 output, the major had to forgo a production ramp up due to the sulfuric acid shortage and development issues.

Analysts and market watchers foresee the sulfuric acid shortage being a long-term price driver.

“The sulfuric acid issue in Kazakhstan is a systemic problem that we do not believe will go away any time soon,” said Finegold. “While the company is doing what they can to alleviate pressures on sulfuric acid supplies, we believe their ability to ramp up production will be hindered for several years before their third domestic plant comes online. As such, we do not see Kazakh uranium production increasing significantly over the next three to four years.”

COP28 nuclear commitment supporting demand

The U3O8 spot price spiked again in early February, reaching US$105 before another correction set in.

As Finegold explained, some of the retraction was the result of profit taking from short-term holders.

“Financial speculators looking to lock in profits towards March year ends played a role, but as we know these moves are achieved on very little volume, so the point remains that the long-term thesis remains unchanged,” he said.

Finegold went on to highlight the different investment perspectives within the market.

“Spot market participants trade on very different parameters and time horizons to one another,” he said. “A trader and a hedge fund, for example, act in a totally different manner to a utility who are long-term thinkers.”

Despite February's slight contraction, uranium prices have remained elevated above US$80.

Some of this long-term support is the result of a COP28 nuclear capacity declaration. At the organization's December meeting in Dubai, more than 20 countries signed a proclamation to triple nuclear capacity by 2050.

There are currently 440 operational nuclear reactors with an additional 13 slated to come online this year and another 47 expected to start electricity generation by 2030. For Finegold, this commitment to building and fortifying nuclear capacity has been uranium's most prevalent demand trend. “The demand side of the equation remains robust and growing at a time when the supply side has never been more fragile,” he commented.